Recently I had an argument with auditors of one company related to the customer list they bought.

The company paid significant amount of cash for the list of customers of telecommunications.

The list contained the names, addresses and phone numbers of all the clients.

And, the buyer intended to use the list to contact the potential customers and offer them their own services.

Well, if it’s ethical or not – I leave that up to you, but the auditors of the buyer said that the price paid for the customer list is an expense in profit or loss.

Is it???

I was not so sure.

To me, the customer list perfectly meets the definition of the intangible asset and in this case after asking few more questions I was sure that the buyer acquired an asset instead of expense in profit or loss.

In today’s article we will look at how to distinguish between intangible assets and expenses and you can find practical illustration in the end.

Including the customer list.

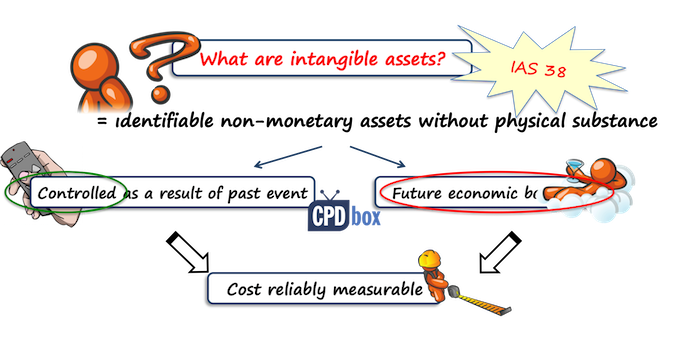

What is an intangible asset?

When I am unsure whether certain item is intangible asset or just an expense, I always look to the basic definition of an asset in IAS 38 and in Conceptual Framework, too:

An asset is a resource controlled by an entity as a result of past events, from which future economic benefits are expected to flow to the entity. (Framework, par. 4.4 (a))

And, IAS 38 expands this definition for intangible assets by specifying that on top of basic definition, an intangible asset is an identifiable non-monetary asset without physical substance.

To sum up, each intangible asset has 3 main characteristics:

- It is controlled by the entity

- No physical substance

- It is identifiable.

Just warning: it can happen that an asset has all 3 characteristics, but you cannot recognize it in your statement of financial position.

The reason is that it still may not meet the recognition criteria.

For example, let’s say you are a telecom company and you have millions of customers.

In this case, you have a customer list that is an intangible asset (please see below for reasoning), but you can’t show it in your balance sheet, because you cannot measure its cost.

Just be aware of these situations.

Now, let me explain shortly what each characteristic means.

1. Controlled by the entity

If you are able to get the future economic benefits from the use of the asset and at the same time, you can prevent others to get these benefits, then you control the asset.

In most cases, you control intangible asset when you have the legal rights to it.

For example, you may have bought the licenses or signed some contract.

Sometimes, control is achieved in a different way.

For example, you may develop some great software internally and you control its sales.

In some cases, you can’t really demonstrate sufficient control of asset and thus you can’t recognize it.

Typical example of such situation is qualified employee – human resources are rarely intangible assets, because you can’t demonstrate control.

2. No physical substance

This one is clear – if some asset has physical substance, then it’s tangible and not intangible.

However, there’s a small exception.

Sometimes, intangible asset is attached to something physical in order to carry it or store it.

In this case, the asset is still intangible because the value of the related physical asset is very small when compared to the value of intangible asset.

3. It is identifiable.

This one is crucial, I think.

The asset is identifiable in one of these 2 cases:

- It is separable – so, you can actually separate the asset and sell it, transfer it, license it or do any other action. Hypothetically.

- Arises from the legal rights – either from contract, legislation etc. In this case, the asset does not need to be separable.

For example, imagine you worked hard and you created a famous brand.

Is it identifiable?

Yes, it is, because you can (hypothetically) license it or sell it.

So, you know what the intangibles are.

From now on, always focus on these 3 characteristics to answer whether you deal with an intangible asset or not.

Can we capitalize the intangible asset?

If it is an intangible asset, then you still have 2 more questions to answer before you capitalize it:

1. Can you measure its cost reliably?

This one is straightforward.

If you can’t measure the cost, then you cannot capitalize even when it is an intangible asset.

I described the example above: you cannot capitalize internally generated customer list because you can’t really determine your cost to develop it.

2. Are the future economic benefits of the asset expected to flow to the entity?

Oh, I love this one.

Future economic benefits can be either increase in revenues or reduction in expenses.

Either way you look at them, the future economic benefits are the potential to increase your profits.

However, many people believe that you must be able to measure them – otherwise they are not the future economic benefits.

No, not at all.

In fact, it is almost impossible.

Imagine you invest in the nicer office, you buy artwork, nice furniture… can you really measure the increase of your revenues as a result of these assets?

No, you cannot, but you are quite sure that nicer office has the potential to pull more money out of the pockets of your clients.

On top of these requirements, there are still some intangible assets that are not intangible assets under IAS 38, but something else.

Important note: The above applies fully to the intangible assets that are NOT under development. If you are developing intangible assets, then you have to meet further 6 conditions to capitalize the expenditures, but let’s touch it in some of my next articles.

Let’s me show you some specific examples.

Examples of intangible assets

Licenses to trade

You operate a taxi service, but you also act as an intermediary for single private taxi drivers to get their own license.

So, as a part of your business you acquire transferrable taxi licenses from the government and you sell some of them to the private drivers who buy from you as it’s easier to get the license this way.

You acquired 1 000 number of taxi licenses.

You employ 400 taxi drivers and you plan to sell another 600 taxi licenses to private drivers.

In this case, all 1 000 taxi licenses are indeed intangible assets, because they satisfy all requirements.

However, you won’t account for all of them as for intangible assets under IAS 38.

Instead:

- 400 licenses used by your own employees are intangible assets; and

- 600 licenses to be sold are your inventories under IAS 2, because you hold them for sale in the ordinary course of business.

Internet websites

The e-shop is famous and attracts a lot of customers. There’s also a section with a company’s blog with articles about the newest fashion trends.

This website is an intangible asset, because yes, the company controls it, it has no physical substance and it is identifiable (i.e. company can sell it).

However, can you recognize it as an asset?

Yes, it brings the future economic benefits, so this one is met.

But, can you measure its cost reliably?

If it was developed externally by the third parties, then yes, you can.

If it was developed internally, then well, you have to apply the rules in IAS 38 and especially in SIC 32 Intangible assets – website costs to determine the capitalization.

Hockey team

The price you paid was derived from the quality and fame of the specific hockey players in that team.

Now, is this hockey team – or better said – contracts with players an intangible asset?

Well, I always say that no, normally you do not capitalize contracts with employees or any other expenses related to employees, because you can’t control them.

In this case, the situation can be different.

For example, hockey players might be prohibited to play in another teams by the legal rules placed by some hockey authority.

Also, the contracts with individual players might legally bind the player to stay with the same team for a number of years.

In this case, you would be able to demonstrate control and yes, recognize hockey team as your intangible asset.

Software licenses

When the computers arrived, you made an online purchase of corresponding number of licenses for Windows XY operating system to run the computers.

Also, you purchased a license to use the specific accounting software.

On top of the purchase cost you are required to pay the annual fee for upgrades of the software. You can continue using the license for accounting software also without annual upgrade fees, but you won’t receive any updates.

Here, we have 3 items:

- Operating system Windows XY

Yes, it is an intangible asset because it meets all the criteria.

However, operating system is an integral part of the computers, because the computers can’t run without the system.

Therefore, you would recognize computers together with operating system as property, plant and equipment, so no separate intangible asset.

For further reference, look to par. 4 of IAS 38.

- Accounting software license

This is an intangible asset, too.

In this case, you need to recognize the license as an intangible asset, because accounting software is NOT essential to run the computer.

- Annual upgrades

Annual upgrades do not meet the definition of an intangible asset, because they are not separable.

They are expensed in profit or loss when incurred.

You can see them as something similar to maintenance and repair costs of property, plant and equipment.

Customer lists

Is this an intangible asset?

In most cases yes, because:

- It has no physical substance,

- It is identifiable (yes, it is because you were able to buy it),

- You control it,

- You can measure its cost reliably (you paid for it) and,

- You expect the future economic benefits (increased sales as a result of new list of potential customers).

I spoke more about it in this IFRS Q&A podcast episode.

Warning: in some countries and at some circumstances such a customer list is not an intangible asset.

The reason is that some countries have legislation in place that prevents you from random contacting the potential customers on the list.

In this case you would not be able to get the future economic benefits from the list because you cannot use it (so why would you buy it anyway?). Thus you do not control the asset fully.

However, telecoms often ask their customers to agree with passing their data to third parties for advertising purposes, so in this case you would be able to use the list (hint – read the small letters in the contracts to know what you agree to!).

You have to assess all of these things to conclude whether the customer list is an asset or not.

Advertising campaign

Some companies invest heavy cash into their advertising campaigns.

Literally millions.

Imagine you plan to invest 1 mil. EUR into the advertising campaign over the next year.

Your advertising agency told you that this campaign would build and strengthen your brand and position in many years to come.

So, some people believe that yes, they should capitalize advertising campaign as it brings the future economic benefits.

No dispute on this.

The only thing is that the advertising campaign is NOT identifiable – you can’t separate it and sell it to someone else.

Therefore, you should recognize the expenditures for advertising campaign in profit or loss.

Of course, when you prepay the campaign for let’s say 2 years, then you should recognize the expenses over 2 years as the services are consumed.

Do you have questions about any other specific items? Please let m know in the comments. Thank you!