IAS 24 Related Party Disclosures

International Accounting Standard 24

Overview of IAS 24

- Issued: in 1984; re-issued in 2003 and 2009, followed by amendments

- Effective date: 1 January 2011

- What it does:

- It helps identify:

- Related party relationships and transactions;

- Outstanding balances between the reporting entity and its related parties,

- When the disclosures should be made.

- It determines what disclosures should be made.

- An entity must present related party disclosures even though there have been no transactions.

- It helps identify:

Main rules of IAS 24

Definition of a related party:

(IAS 24.9)

- A person or a close member of that person’s family is related to a reporting entity if that person:

- Has control or joint control over the reporting entity;

- Has significant influence over the reporting entity; or

- Is a member of the key management personnel of the reporting entity or of a parent of the reporting entity.

- An entity is related to a reporting entity if any of the following applies:

- The entity and the reporting entity are member of the same group.

- One entity is an associate or joint venture of the other entity (or a group).

- Both entities are joint ventures of the same third party.

- One entity is a joint venture of a third entity and the other entity is an associate of the third entity.

- The entity is a post-employment defined benefit plan for the benefit or employees of either the reporting entity or an entity related to the reporting entity. If the reporting entity is itself such a plan, the sponsoring employers are also related to the reporting entity.

- The entity is controlled or jointly controlled by a person identified in (1).

- A person identified in (1)(i) has significant influence over the entity or is a member of the key management personnel of the entity (or of a parent of the entity).

- The entity, or any member of a group of which it is a part, provides key management personnel services to the reporting entity or to the parent of the reporting entity.

Disclosures required by IAS 24

- Relationships between parents and subsidiaries:

- Name of a parent of an entity,

- The ultimate controlling party,

- Next most senior parent that produces financial statements for public use (if neither of 2 above do so).

This must be disclosed even if there are no related party transactions.

- Management compensation, both total and by the categories:

- Short-term employee benefits,

- Post-employment benefits,

- Other long-term benefits,

- Termination benefits,

- Share-based payment benefits

- Related party transactions

These represent any transfer of resources, services or obligations between related parties regardless of whether a price is charged (IAS 24.9).

An entity should disclose:- Nature of the relationship and

- Information about transactions and outstanding balances

The disclosures are presented separately for each category of related parties and include (IAS 24.18):

- Amount of transactions;

- Amount of outstanding balances, together with:

- their terms and conditions (are they secured? What consideration is to be provided in settlement?), and

- guarantees.

- Provisions for doubtful debts related to the amount of open balances; and

- The expense during the period for bad or doubtful debts due from related parties.

Examples related to IAS 24

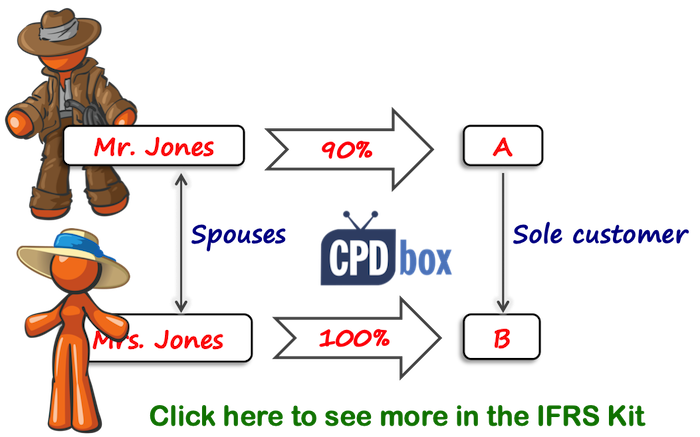

Example 1: Close family members

A major shareholder of an entity A, Mr. Jones has a wife who owns an entity B. An entity B is a sole customer of an entity A, but there is no ownership of an entity B by an entity A or vice versa.

Who are related parties of an entity A?

Solution

Major shareholder and his wife are related parties, because they are a person or a close family member of that person (wife) who control the entity A.

Entity B is a related party of an entity A, because it is controlled by close family member of a major shareholder of A (not because it is the sole customer).

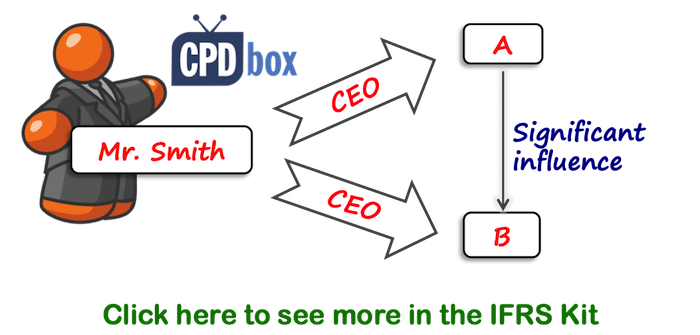

Example 2: Key management personnel compensation

Entity A has an associate, entity B, over which it has significant influence. Mr. Smith is a CEO of both A and B and shares his time 50% with entity A and 50% with entity B.

Both A and B pay him a salary for the services provided and he has separate contracts with both A and B.

What should A disclose in terms of remuneration paid to Mr. Smith?

Solution:

A should disclose only the remuneration paid to Mr. Smith by A, and not include remuneration paid by B.

The reason is that IAS 24 requires disclosing remuneration for services paid by the entity for services rendered to the entity – thus to A only.

Also, B is only associate, thus not part of the group (which is defined as a parent and its subsidiaries by IFRS 10.)

If A is a parent and B is a subsidiary, then in the consolidated financial statements of A group, total remuneration paid by both A and B would need to be disclosed.

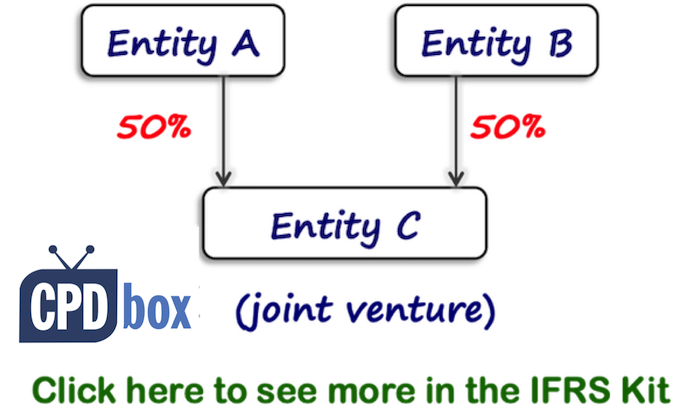

Example 3: Joint venture

The company A and the company B established a joint venture C. Each A and B have 50% share.

Who is a related party to A?

Solution:

The joint venture C is a related party to A, because it is under joint control of A.

The company B is NOT a related party to A.

For more examples, please refer to the IFRS Kit.

Other Resources

- IFRS Kit - learn IFRS in 150+ videos, 150+ excel case studies, quizzes, certificates

- Expected Credit Loss for Accountants - highly specialized course focused on ECL under IFRS 9 with step-by-step example related to trade receivables, many practical insights included.