How to classify expenses in profit or loss statement under IFRS?

How to classify expenses in profit or loss? And, what to do when you have to change this classification?

Where to present depreciation? Salaries?

Let’s see today’s question:

“Dear Silvia, I am auditing a company who owns warehouses in several locations and rents the warehouses to other companies.

Last year, the company’s owners changed and as a result, there was a change in company’s operations.

Before, employees were assigned to the specific warehouse and worked in that warehouse only.

Now, employees rotate and can serve more warehouses over some time period.

On top of it, few administrative employees were fired and warehouse employees work on admin tasks, too.

So, we have a problem with classification of expenses.

Before, all salaries of warehouse employees were classified as cost of sales because they worked in warehouse.

Now, after the change, these salaries are classified simply as personnel expenses and as a result, cost of sales dramatically decreased.

How to solve this situation? Is this OK?”

IFRS Answer: Classification and its change

I like this question, because it deals with two issues:

- Classification of expenses in profit or loss, and

- Change in presentation of your profit or loss.

Classification of expenses in profit or loss

I often receive questions like:

- How to present depreciation expenses?

- How to present insurance of offices? And similar.

Let me say that you have a choice here.

The standard IAS 1 Presentation of financial statements does NOT prescribe how you should present your expenses.

In fact, there is NO mandatory format.

The reason is that every single entity is different in its activities and shows different profile of expenses necessary to achieve revenues.

Therefore, the standard requires the presentation of expenses in profit or loss in a way that provides more reliable and relevant information about your own activities.

It is true that the standard IAS 1 suggests 2 different formats:

- Expenses by nature and

- Expenses by function.

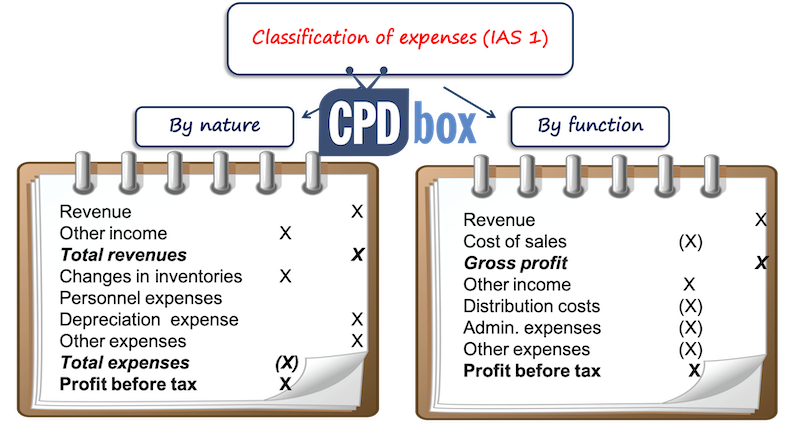

Expenses by nature

When you present by nature, then you simply group the expenses by their nature regardless the role that they play in your company.

You do NOT reallocate them among various functions in your company.

For example, the salary of warehouse employees and the salary of admin employees will be presented as personnel expenses.

Similarly, depreciation of warehouse and depreciation of admin building will be presented as depreciation expenses.

The big advantage of this method is that it is very simple because you don’t have to worry with allocations.

Expenses by function

Here, you group your expenses by the functions in your company.

For example, salary of warehouse employees and depreciation of warehouse are presented as cost of sales.

Salary of admin employees and depreciation of admin building are presented as administrative expenses.

This method is more demanding because it requires certain work and judgment when reallocating your expenses among various functions, but it is probably more relevant for some types of companies.

What classification to use?

And now, let me clarify that IAS 1 DOES NOT require analysis of expense by function or by nature on the face of profit or loss statement – it is a suggestion.

In fact, you are permitted to disclose the classification on the face of the profit or loss statement on some mixed basis.

For example, you present cost of sales as a function, then you present gross profit and then you present depreciation expenses – this is an element from by nature method. That’s the illustration of the mixed basis.

What about the change in presentation?

Let’s get back to the first part of today’s question:

It is OK to present salaries of employees as cost of sales to the extent they relate to their warehouse work.

And, it is also OK to present these salaries as personnel expenses, if this is more relevant for the company’s activities.

But here, the question contains one more element: change in presentation.

One year, the expenses were presented as cost of sales and another year, they were presented as personnel expenses.

Well, this is not permitted.

Instead, you should bear in mind another two requirements of IAS 1:

- Consistency of presentation.

You need to retain the presentation and classification of items in the financial statements from one period to the next.You can change the presentation, but only when there is a change in entity’s operations and the new way of presenting would be more relevant.

Or, when IFRS standards change.

- Comparative information

If you make the change in presentation, you need to reclassify your comparative information, too.

It means that if you presented salaries of warehouse employees as cost of sales in the previous period, and now you want to present them as personnel expenses – you can do it, but you need to reclassify these salaries in the previous reporting period to personnel expenses too in order to make previous and current numbers comparable.

So, the company from today’s question needs to present the profit or loss from the previous period in a new format and thus the cost of sales won’t dramatically decrease and the two statements will be fully comparable.

Here’s the video summing up the issue:

Any comments or questions? Please let me know below – thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

23 Comments

Leave a Reply

Thanks so much for Sharing it is so insightful

Well guided

One of your simplest articles you still make it easy …. thank you

Hi Silvia! How to account technical maintance of leasing objects? We are lessor of ships. There is a new agreement (not a part of leasing agreement!) with third party that will maintence ships on regular bases. Is it other expense for us or no? What do you think?

Hi dzirt, well, it depends on what the lease contract says – is maintenance of the ships included in the price of lease? Will lessee refund the maintenance? I cannot really assess based on this short info.

Thank you for the post.

To me expenses by nature give clear indication of “trends”. One may have by function classification for management reporting, down to the departments / responsibility accounting.

e.g. Fuel prices are increasing will be visible in by nature classification while will be lost in by function classification.

However by function classification will required for closing inventory valuation in manufacturing concerns. In Pakistan we have two groups on face of Income Statements; Cost of goods sold and “Selling Admin expenses” with by nature classification in two notes.

I agree with you. When you do “by function”, it is quite judgemental and yes, can hide anything, but the point is to be consistent and fair. Thank you!

Hi Silvia,

Thank you for the reply. I appreciate it.

Hi Silvia,

thank you so much for sharing the above info. I have a question W maybe you can help me. Why do you think the IASB is considering requiring companies to use either the Nature of expense method or the Function method of expense?

Hi Marjorie, just for the sake of some order in presentation.

Silvia, Thanks for the wonderful explanation.

Hello Silvia,

I heard someone mention that you can’t present name expense/(income) non-operating expense/(income) and you can only use operating expense/(income). Is this true ? And if yes how do you disclose income or expense that are not operating ? for example write-off or insurance received ?

Hi Ronald,

I think you heard that you cannot use “extra-ordinary” expense/income, because even earthquakes are a part of operations, isn’t it? You can have non-operating expense, for example interest paid can be presented as such.

Thank you very for your explanation. It is very useful!!!

thank you very much!!! it is help me a lot !!!

Hi, Dear Silvia

Many thanks for the nice clarification.

I have a question in this regard. As you said to make consistency in comparison, expenses may be reclassified. In such a situation, if the reclassification becomes material, shouldn’t we apply retrospective accounting or just give a disclosure is enough?

Hi Robiul, I would say that the classification of expenses is more-less disclosure issue, not the recognition itself. Having that said – that’s why you are presenting the comparatives under the new classification, too (it is a kind of restatement).

Dear Silvia, I am a first year business student at university in Australia.

For one of my assessable homework questions it asks us to prepare an income statement.

it specifically states to NOT CLASSIFY THE EXPENSES.

i’m a bit lost on what that actually means…..could you please explain a little bit on what that actually means.

Thank you.

Simple but informative.

Thank you for making it so

Dear Silvia,

It is really helpful, i like the way in u explain the topic very easily,,,, so good. Thanks

Best wishes.

Dear Silvia ,

It’s really helpful thanks for your explanation.

Regards,

Rana Atif

Hello I really like they youe explain please explain with few example accounting treatment of intangible assets,cash flow statement , partnership and leases

Silvia,

Thank you very much for the input, it is very helpful.

Stay blessed.