Coronavirus and IFRS – What is happening?

Over past few months, coronavirus became the most mentioned word everywhere. No wonder – not only it takes lives of our dear ones, but it also affects our daily life in many different ways. In many countries, people cannot go to work, kids cannot go…

How to Measure Fair Value in Agriculture – IAS 41 and IFRS 13

Agriculture is a huge sector, significantly contributing to the world’s GDP. According to the World Bank, in 2018 the value added in the agricultural sector represented 10.39% on total GDP in average – which is HUGE! After all, we all need to eat. Besides its…

Example: IAS 33 EPS and Rights Issue

Step-by-step calculation of earnings per share in line with IAS 33 for the rights issue.

{kind=link}

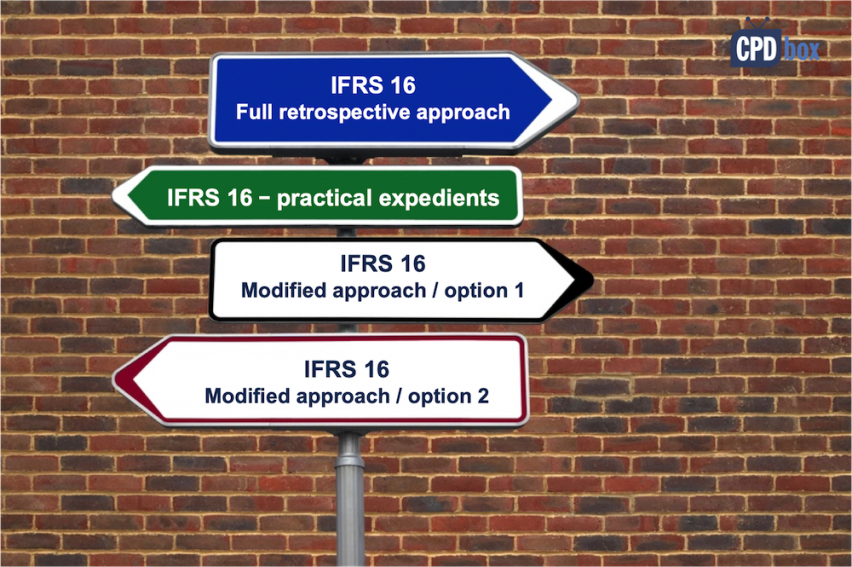

Adopting IFRS 16 – What Is The Best Option For You?

Let’s compare different transition options that you have when adopting IFRS 16 in your company. Let’s see what they are, which one is easier and which one has the smallest impact on your equity.

Conceptual Framework for the Financial Reporting 2018

The summary of the Conceptual Framework for Financial Reporting 2018 – with VIDEO!!!

How to make a change in functional currency

Some time ago I was a part of an audit team auditing the financial statements of a medium-sized manufacturing company. When we received the trial balance of that client, we spotted something strange: There were loads of transactions in a foreign currency and resulting impact…

IFRS 2019 Update: Major changes you should be aware of

Here we go again – another year has started and a number of changes or amendments of IFRS came into effect. I am pretty sure that you are aware of the biggest ones like new IFRS 16, but let me sum up all the new…

Example: IFRS 10 Disposal of Subsidiary

Updated 2025: Disposal of a subsidiary step-by-step under IFRS 10 lecture: Some time ago I published an article with an example of very simple method of consolidating a parent and a subsidiary. This article still applies and you can learn the basic steps and methodology…

How to Consolidate Special Purpose Entity

Last update: 2023 I lost my first serious job in Arthur Andersen in 2001. I was devastated, because I really loved that job. Yes, it was full of hard work and long overtimes, but it was the best accounting and auditing school ever. How did…

{kind=link}

How to Present Earnings per Share (IAS 33)

If you invest your savings to the purchase of some shares on the stock exchange, then you probably perform some analysis in order to select the right stock. Well, this is at least what you should do. Still, your own hard-earned money needs to work…