IFRS 9 Hedge accounting example: why and how to do it

Hedge accounting is an optional model for reporting the derivatives, yet it is not a free ride: there are conditions and admin work to do.

So, if there is so much additional work related to hedge accounting, why even bother?

Well, some people say that hedge accounting is a privilege that we must earn.

Let me show you why and how to do that here:

- What is hedging and hedge accounting?;

- Types of hedges;

- Hedge accounting example: a forecast sale;;

- Let’s compare: with or without hedge accounting?;

- Video lecture: Hedge accounting example

What is hedging and hedge accounting?

Let’s see the case

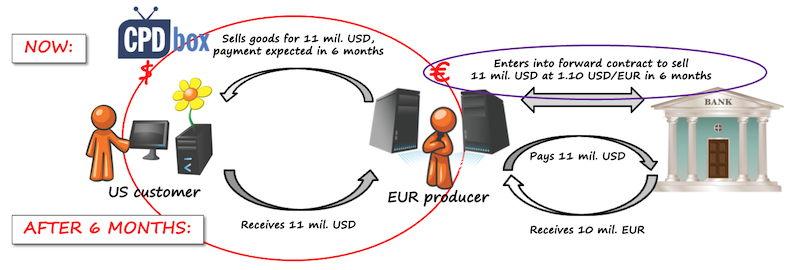

Imagine there’s a European producer whose functional currency is EUR.

That producer finds a customer in the USA (with USD as a functional currency) and agrees to sell the goods for the total amount of 11 mil. USD. The sale is expected in 6 months.

So, there’s a foreign currency risk because within those 6 months, the exchange rate of USD/EUR can shift to either direction.

To protect against this risk, the EU producer enters into the foreign currency forward contract with the bank to:

- Sell 11 mil. USD, and

- Buy 10 mil. EUR

in 6 months.

Therefore, EU producer effectively fixed the exchange rate to 1.10 USD/EUR and know exactly what amount of EUR it will receive for the products sold to the US customer.

After 6 months, the spot rate applicable on the market is 1.15 USD/EUR.

See what happens:

- EU producer delivers the goods to the US customer and gets 11 mil. USD;

- EU producer translates those 11 mil. USD to EUR by the spot rate of 1.15, thus getting 9 565 217 EUR;

- At the same time, it pays 11 mil. USD (translated by the spot rate to 9 565 217 EUR) to the bank;

- And receives 10 mil. EUR from the bank.

Therefore, as a result of a foreign currency forward contract, EU producer received 10 mil. EUR, and not 9 565 216 EUR for its 11 mil. USD. This is hedging in practice.

Of course, the rates can shift the other direction, causing the producer to receive less EUR for 11 mil. USD that would have been received at the spot rate.

Let me just remind you that sometimes, the purpose of hedging is NOT to make profit, but to FIX future cash flows.

What is hedge accounting?

Hedge accounting is designating one or more hedging instruments, so that their change in fair value is an offset to the change in fair value or cash flows of the hedged item.

So, we have two items here:

- Hedged item: this is an item that carries certain risk. It could be a recognized asset or liability, an unrecognized firm commitment, a forecast transaction (anticipated sale or purchase) or a net investment in a foreign operation.

- Hedging instrument: a derivative (or some other non-derivative financial asset or a non-derivative financial liability) whose fair value changes are expected to offset the fair value changes of a hedged item.

Simply said, if there is a loss on hedged item, there will be a gain on hedging instrument to offset that loss.

And the opposite is true: if there is a gain on hedged item, there will be a loss on hedging instrument.

In our short illustration:

- The hedged item is highly probable forecast sale in foreign currency;

- The hedging instrument is a foreign currency forward contract.

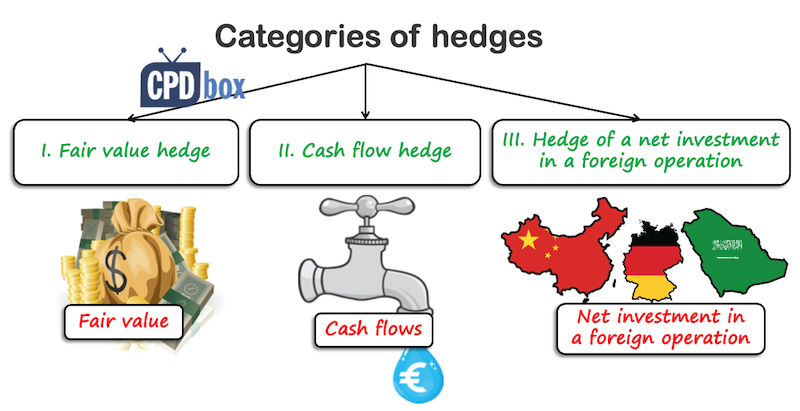

Types of hedges

There are three types of hedges in IFRS 9:

- Fair value hedge;

- Cash flow hedge;

- Hedge of a net investment in a foreign operation.

To most foreign currency hedges, a cash flow hedge is applied (although you can do fair value hedge, too, in most cases).

Cash flow hedge

Cash flow hedge is a hedge of the exposure to the variability of cash flows that could affect profit or loss.

If the hedge accounting criteria are met, then the accounting for the derivative (hedging instrument) is as follows:

- Its fair value gain or loss is split into two parts:

- The effective part: this is the part which perfectly offsets the fair value change on hedged item and it is recognized in other comprehensive income as a cash flow hedge reserve.

- The ineffective part: the remaining part of the fair value change of the derivative (hedging instrument) is recognized in profit or loss.

- The accumulated cash flow hedge reserve is accounted for in one of the two ways:

- If the hedged forecast transaction results in a subsequent recognition of a non-financial asset or a non-financial liability, it is included in the cost or other carrying amount of that asset or a liability;

- When the hedged item affects profit or loss, the cumulative cash flow hedge reserve is reclassified to profit or loss as a reclassification adjustment at the same time.

Let’s explain that on an example.

Return to top

Hedge accounting example: forecast sale

The transaction is as follows:

- The functional currency of an entity is EUR;

- The sale of 11 mil. USD is expected in 6 months;

- Start date: 1 December 20X4, end date: 31 May 20X5;

- To protect against foreign currency risk, the entity enters into a foreign currency forward contract with the bank to sell 11 mil. USD for 10 mil. EUR on 31 May 20X5;

- On 31 December 20X5, fair value of the forward contract is a gain of 150 000 EUR; fair value of the anticipated sale is a loss of 150 000 EUR; there is no ineffectiveness for simplicity;

- Spot rate at sale on 31 May 20X5 is 1.15 USD/EUR;

Journal entries when NO hedge accounting is applied

If the entity decides not to apply hedge accounting, then it still needs to recognize the change in fair value of the derivative in profit or loss (IFRS 9).

Journal entry at the end of 20X4 is as follows:

- Debit Derivative assets: 150 000 EUR

- Credit P/L – FV gain on forward contract: -150 000 EUR

At the time of the sale on 31 May 20X5, it is necessary to calculate the fair value of the derivative first and recognize its fair value gain or loss.

Calculation:

- To sell 11 mil. USD at the spot rate of 1.15 USD/EUR, the entity would receive 11 mil. USD / 1.15 = 9 565 217 EUR;

- To sell 11 mil. USD at the contracted forward rate, the entity would receive 10 mil. EUR (which is more beneficial than above);

- Total gain: 10 000 000 – 9 565 217 = 434 783 EUR;

- Less already recognized in 20X4: 434 783 – 150 000 = 284 783 EUR

The journal entry is as follows:

- Debit Derivative assets: 284 783 EUR

- Credit P/L – FV gain on forward contract: -284 783 EUR

Also, the forward comes to its maturity, so the entity must account for its settlement with the bank. The journal entry is as follows (gross settlement):

- Debit Bank accounts: 10 000 000 EUR – this is the amount received from the bank;

- Credit Bank accounts: -9 565 217 EUR – this is the amount of 11 mil. USD paid to the bank, translated at the spot rate;

- Credit Derivative assets: -434 783 EUR – to derecognize the derivative asset since the derivative terminated.

Of course, the entity would then recognize the regular sale transaction at the spot rate:

- Debit Trade receivables: 9 565 217 EUR

- Credit P/L – Revenues from sales: -9 565 217 EUR

Journal entries when hedge accounting IS applied

This time, the entity did all the admin work and met the conditions to apply the cash flow hedge accounting.

At the year-end on 31 December 20X4, the forward contract is revalued as follows:

- Debit Derivative assets: 150 000 EUR

- Credit OCI – Cash flow hedge reserve: -150 000 EUR

Since there was no ineffectiveness, there is nothing to recognize in profit or loss.

When the sale happens on 31 May 20X5, there are three entries to make:

- Revaluation of hedging instrument to its fair value: The calculation is the same as before when no hedge accounting was applied, but this time, the full gain is recognized as cash flow hedge reserve in other comprehensive income. The entry is

- Debit Derivative assets: 284 783 EUR

- Credit OCI – Cash flow hedge reserve: -284 783 EUR

- Settlement of forward contract with the bank: This is exactly the same entry for the gross settlement as when no hedge accounting was applied.

- Debit Bank accounts: 10 000 000 EUR

- Credit Bank accounts: -9 565 217 EUR

- Credit Derivative assets: -434 783 EUR

- Transfer of cash flow hedge reserve to profit or loss, because the hedged item (sale) affected profit or loss. The entry is

- Debit OCI-Cash flow hedge reserve: 434 783 EUR

- Credit P/L-Revenues from sales: -434 783 EUR

And again, we need to recognize the regular sale transaction at the spot rate:

- Debit Trade receivables: 9 565 217 EUR

- Credit P/L – Revenues from sales: -9 565 217 EUR

Let’s compare: with or without hedge accounting?

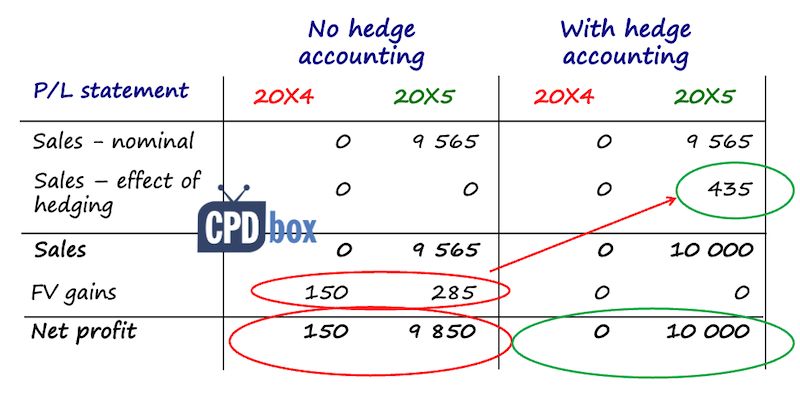

Let’s see how the transaction looks in the financial statements and compare two different accounting treatments.

Please note that the following table shows only the effects of the transaction, not the full profit or loss statements:

We can see clearly that:

- With hedge accounting, gain from the foreign currency forward contract is shifted to and reported in the same reporting period as the hedged item. It is not spread to two reporting periods as if no hedge accounting was applied.

- With hedge accounting, gain from the foreign currency forward is presented together with the hedged item, as revenues from sales. This reflects the risk management strategy. If no hedge accounting is applied, the gain from forward contract is shown below as some financial result.

As a conclusion: Yes, hedge accounting involves more administrative work and calculations, but it shows the management of risks rather than some “random” derivatives in the financial statements.

Also, volatility in profit or loss is lower.

Return to top

Video lecture: Hedge accounting example

You can watch the free lecture on hedge accounting here:

This is the full lecture from the IFRS Kit which contains contains the full video lectures with many practical examples solved in Excel that will guide you, step by step, through the financial instruments and their accounting.

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

6 Comments

Leave a Reply

Why would the forward contract run past the transaction date? The dates don’t make much sense.

if i subcribe do i get to ask questions to an expert

this is quite helpful…..you are a star

how about an example of hedging a foreign current cash flow payment for AP

Good Explanation

Great explanations!!, thanks