Projected Unit Credit Method (IAS 19) with Example

Recently I got across the interesting question.

One lady working for a company adopting IFRS for the first time asked me if they can still mark their financial statements as compliant with IFRS, if they do not apply projected unit credit method, but do apply everything else.

In her view, it was extremely difficult and not worth it.

Hmmm.

The method itself is not that difficult to apply once you have the correct inputs (or information).

Let me show you. Hint: Watch the video + download the excel file at the end of this article.

Projected Unit Credit Method: Basics

Projected Unit Credit Method is required by the standard IAS 19 Employee Benefits in accounting for defined benefit plans.

Once an employer provides some employee benefit to its employee(s) and this benefit is classified as defined benefit plan, then the employer must apply this method to measure:

- Present value of defined benefit obligation: that is, in simple language, the amount that the employee earned for his service from start of his employment contract till the current reporting date stated in present value;

- Current service cost: this is the amount that the employee earned for his service in the current reporting period (which adds up to the defined benefit obligation);

- Past service cost: if there is a change of plan and the employee will get greater/lower benefit also for the previous reporting periods; then past service cost represents the amount to reflect changes for the past. However, we will skip it in this basic explanation, but if you wish to learn more, the full lectures are in the IFRS Kit.

Imagine you have a contract with the employee for 7 years, from 1 January 20X1 to 31 December 20X1 and on top of his salary, the employee will receive one-time bonus at the end of his employment amounting to CU 300 000.

Let’s say this bonus is a motivation offered right in the employment contract and will be paid only at the end of the employment, so you classify this bonus as a defined benefit plan.

What NOT to do:

- Do not accrue all amount in profit or loss in 20X7!

Your employee earned this amount over 7 years, not solely in the year 20X7 and the main principle is to recognize the cost in the period when the employee works, so over 7 years. - Do not divide CU 300 000 by 7 and recognize that amount in profit or loss each year!

It is wrong, too. While it is closer to the correct method, but it’s still wrong, because you are ignoring the time value of money and other assumptions.

Instead, apply projected unit credit method.

How to apply the projected unit credit method

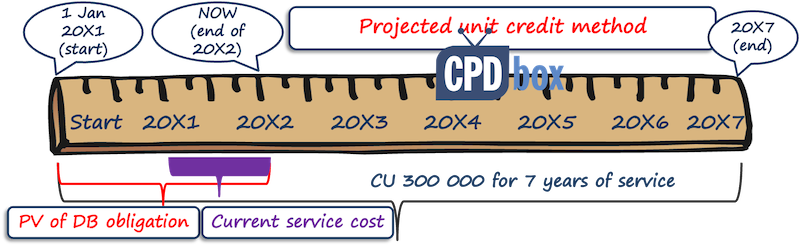

In the following picture, there is the employment timeline, starting from 1 January 20X1, ending at 31 December 20X7 and as you can see, the bonus of CU 300 000 is earned over all period.

In the timeline, imagine we are at the end of 20X2 – that’s labelled as “NOW”.

Present value of defined benefit obligation at the end of 20X2 (NOW) is marked in red; current service cost for 20X2 is marked in purple.

We are going to apply projected unit credit method to measure these 2 amounts.

Before we solve the example, let me add two notes to this method:

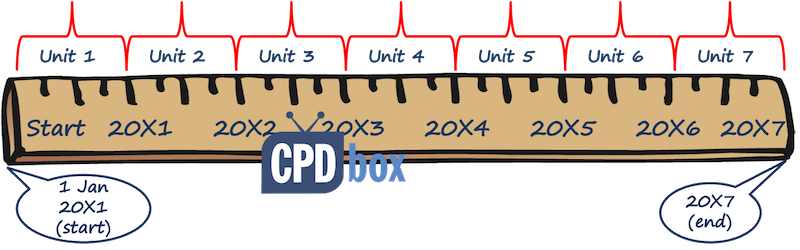

- When you apply the projected unit credit method, the defined benefit obligation gradually builds up over the period of service. So no accruing the full amount in one period. Instead, each year of service adds some part to the final benefit obligation. We call this part a unit

- You need to measure each unit separately to reflect time value of money and other aspects; thus it will not be the same each year.

Example: Projected Unit Credit Method

Let’s take the same employment contract as above:

- Term: 7 years

- Start date: 1 January 20X1

- End date: 31 December 20X7

- One-time bonus at the end date: CU 300 000

- Discount rate: 2%

- Ignore all other actuarial assumptions.

Before we start working, let me remind you – you have to classify your benefit first.

We assume here this is the defined benefit plan. If it’s something else, then you do not apply this method, but go according to what it is. IAS 19 will tell you.

Step 1: Estimate the ultimate cost of benefit

First of all, let’s set the ultimate cost of benefit – this is the amount that the employer will actually pay to the employee when the time comes.

In this example, it is very easy: CU 300 000.

Sometimes it’s not that clear because employer can promise to pay some amount depending on future salary.

For example, an employee can get some multiple of its salary at the time of retirement as a bonus.

Here you would need to estimate what salary the employee will have at the time of retirement and it may not be so easy if the employee is young and will not retire earlier than in 20 years. Also, will this employee stay with your company until his retirement?

This is the reason why actuarial assumptions (like inflation rate, fluctuation rate, mortality, etc.) enter into calculations, but not right now in this simple example.

Step 2: Attribute ultimate cost to the periods of service

We must spread this benefit over employee’s total service – 7 years.

We can attribute the benefit equally to all periods of service here, so to each year of service, we attribute CU 300 000/7 = CU 42 857.

I have done this in the following table:

Please note that the amount earned for previous periods is simply total brought forward from prior year.

As you can see, total benefits at the end of final year of service – 7 or 20X7 – represents 300 000 CU – that is a benefit promised to this employee.

However, that’s NOT the end, because all amounts are undiscounted, not in their present value.

Step 3: Measure each unit separately by discounting it to present value

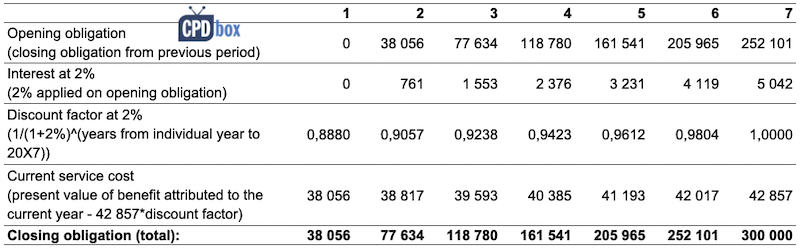

I have done this in another table. Let me explain in a few points:

- The first line represents the opening obligation as at the beginning of the current reporting period.

- In the year 20X1, it’s 0, because the employee started to work for in 20X1.

- In the years to follow, the opening obligation is simply the closing obligation from the previous reporting period. For example, the opening obligation in the year 20X2 equals closing obligation from the year 20X1.

- The second line calculates the interest cost to bring the obligation to its present value at the end of reporting period. Interest cost is calculated as our discount rate (2% in this example) multiplied by the opening obligation.

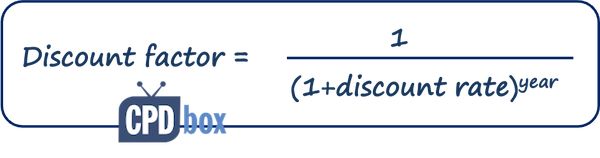

- In the third line, we calculated discount factor at 2%, because we will need it to calculate current service cost.

The formula is shown in the picture below, just let me explain what the “year” means.

It is the number of years from “now” (whatever period you are in) until the end of employment. Thus if you are calculating the discount factor for 20X1, then the year parameter is 6, which is the number of years to go from the end of 20X1 till the end of 20X7 (yes, it is six: 20X2, 20X3, 20X4, 20X5, 20X6 and 20X7).

- The fourth line represents current service cost. It is one unit of benefit spread over full working period of 42 857 CU (see step 2) discounted by the discount rate to its present value.

So, multiply CU 42 857 with the discount factor from the third line. - The last line is the closing obligation as at the end of the current reporting period. It is calculated as

- the opening obligation (first line) plus

- the interest cost (second line) plus

- the current service cost.

At the end of 20X1, the closing obligation represents just 38 056 CU since there was neither opening obligation nor interest cost.

In the subsequent years, closing obligation gradually builds up as there are some interest costs and current service costs each year.

Just look to the end of 20X7 – final year of employment. You can see that present value of obligation is exactly 300 000 CU – the amount to be paid to our employee.

Step 4: Journal entries

In each year, an increase in obligation caused by interest and current service cost is debited to profit or loss account – expense for employee benefits and credited to liability from employee benefits.

For example, in the year 20X1, the journal entry is:

-

Debit Expenses in profit or loss (employee benefits): CU 38 056

-

Credit Liabilities – provision for employee benefits: CU 38 056

Projected Unit Credit Method: video and excel file

You can watch the video with me doing all the workings in excel here:

CLICK here to download the excel file.

Any comments or questions? Please let me know below. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

14 Comments

Leave a Reply

Hi Slivia,

In your example, if the employee gets after joining 300,000 at any time of leaving service during the 7 year contract. Does this mean that the Unit cost shall be 300,000 from year one (will be discounted based on expected time of leaving service)?

Well, this is highly unlikely scenario, because the employee can stay for 1 month and then get the bonus – is that what you had in mind? If yes, then strictly speaking, there is no future service required from him, no vesting and so the bonus is provided unconditionally – therefore, yes, current service cost would be 300 000 at its present value.

Please how was the first line calculated

Iam just mindblown… very clear and precise…thankyou so much☻♥

Thankyou, it really helps

May we also book here the interest like a financial expense as an alternative to operating expence?

Hello could you plz elaborate on the concept of time value of money in employee benefits.

When employee benefits are provided much later (more than 12 months) after the end of the reporting period in which employee provided the service, they must be discounted to present value. That’s it.

why we need to have a discount rate? Is it to show that our cash flow not provide a big provision for the current year

Today’s 1 Rs is greater than 1 Rs after 1 year and that’s called Time Value of Money. Since, the actual paying liability is after some defined years, the amount that will be paid at that time must be lower as if we compare it today. Hence, this is for better presentation prescribed by AS 19.

Thanks for the explanations. Please do let me know the difference between the discount rate and the interest rate. Are these the bank rates or zero-coupon bond rate?

The discount rate is the interest rate at which you discount some cash flows (in this case future “current service cost” attributed to individual periods etc.). In most cases, you need to derive the discount rate from high-quality corporate bonds with similar maturity as the expected time to payment of the benefit obligation. But, if these are not available, you can use government bonds.

So what is the answer to the question in the beginning? Can they mark FS as compliant with IFRS?

No, they cannot – see IAS 1.16. 🙂