Summary of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations

When a company (or another entity) plans to sell an asset and / or stop some part of its business, then it might affect its future cash flows, profitability and overall financial situation.

Therefore, the users of financial statements, mainly investors, should be informed about these events.

That’s why the standard IFRS 5 Non-Current Assets Held for Sale and Discontinued Operations was issued – to highlight the results of discontinued operations and to separate them from the results of ongoing or continuing activities.

So, if you or your company plans to sell some non-current assets and discontinue some operations, then IFRS 5 is for you.

The only exception is when a company regularly sells assets normally considered as non-current. In this case, these sales represent one of primary activities and the related assets are inventories in fact. For example, a car dealer presents all vehicles for resale under IAS 2 Inventories, not under IFRS 5.

Let’s take a closer look to the main IFRS 5 rules.

Objective of IFRS 5

IFRS 5 focuses on 2 main areas:

- It specifies the accounting treatment for assets (or disposal groups) held for sale, and

- It sets the presentation and disclosure requirements for discontinued operations.

Let me point out that you should apply IFRS 5 for all non-current assets – no exception.

The standard IFRS 5 lists some measurement exceptions and you can read about them in the later paragraphs, but you still need to present and disclose the information about these assets under IFRS 5.

When to classify an asset as held for sale

You should classify a non-current asset as held for sale if its carrying amount will be recovered principally through a sale rather than continuing use.

The same applies for a disposal group.

Disposal group is a new concept introduced by IFRS 5 and it represents a group of assets and liabilities to be disposed of together as a group in a single transaction.

For example, when a company runs a few divisions and decides to sell one division, then all assets (including PPE, inventories, deferred tax, etc.) and all liabilities of that division would represent a disposal group.

What if we abandon an asset?

The question is whether you should classify a non-current asset as held for sale in the case when you plan to stop using it, or abandon it.

The answer is NO.

Why?

Because, you will recover its carrying amount through asset’s continuing use and not sale.

What does it practically mean?

Well, it means that you will NOT apply “held-for-sale accounting”, i.e. you will NOT keep an asset at lower of fair value less costs to sell and its carrying amount (as specified below).

But, it also means, that you WILL need to assess the criteria for presenting the abandoned asset or operation as discontinued operation.

When will an asset be recovered through a sale?

In other words, what are the conditions for classifying an asset as held for sale?

First of all, the asset or disposal group must be available for immediate sale in its present conditions and the sale must be highly probable.

IFRS 5 sets a few criteria for the sale to be highly probable:

- Management must be committed to a plan to sell the asset;

- An active program to find a buyer must have been initiated;

- The asset must be actively marketed for sale at a price reasonable to its current fair value;

- The sale is expected to be completed within 1 year from the date of classification;

- Significant changes to the plan are unlikely.

The similar criteria also apply to assets held for distribution to owners.

How to account for assets held for sale

Once you classify an asset or a disposal group as held for sale, then you should measure it under IFRS 5.

However, IFRS 5 lists a few measurement exceptions (IFRS 5.5):

- Deferred tax assets (IAS 12 Income Taxes).

- Assets arising from employee benefits (IAS 19 Employee Benefits).

- Financial assets within the scope of IFRS 9 Financial Instruments.

- Non-current assets that are accounted for in accordance with the fair value model in IAS 40 Investment Property.

- Non-current assets that are measured at fair value less costs to sell in accordance with IAS 41 Agriculture.

- Contractual rights under insurance contracts as defined in IFRS 4 Insurance Contracts.

When you classify any of the above types of assets as assets held for sale, you continue measuring them under the same accounting policies as before classification (e.g. financial instrument held for sale will still be measured under IFRS 9, not IFRS 5).

Why have we classified these assets as held for sale though?

The reason is that although you don’t change their accounting treatment, you change their presentation and disclosures. You will still need to present these assets separately from others and disclose some additional information.

All other assets not excluded in the above list must be measured at lower of their carrying amount and fair value less costs to sell. That’s the main measurement principle of IFRS 5.

How to do it?

Measurement after classification

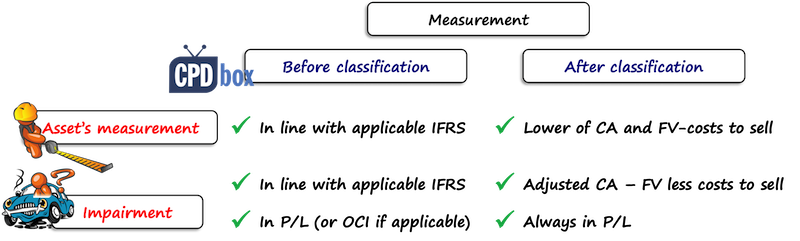

Immediately before you classify an asset as held for sale, you should measure it under applicable IFRS. For example, you would measure an item of property, plant and equipment under IAS 16.

Subsequently, after you classified an asset as held for sale, you should measure it at lower of its carrying amount and fair value less costs to sell (except for measurement exceptions listed above).

Impairment

With regard to any impairment, immediately before classification as held for sale, the impairment is recognized in line with the applicable IFRSs, for example, under IAS 36 for property, plant and equipment.

In this case, you would recognize any impairment loss in profit or loss, but sometimes also in other comprehensive income – that’s when you apply revaluation model for your property, plant and equipment and you have a revaluation surplus to decrease.

After you classify an asset as held for sale, you would recognize any impairment loss in profit or loss only.

What are discontinued operations

IFRS 5 specifies that you need to pay special attention to presenting any discontinued operation. But, what is it?

It is a component of an entity (understand: a cash-generating unit or a group of cash-generating units) that either has been disposed of or is classified as held for sale, and at the same time:

- Represents a separate major line of business or geographical area of operations,

- Is part of a plan to dispose it of, or

- Is a subsidiary acquire exclusively with a view to resale. (IFRS 5.32)

How to present discontinued operations

Once you identify a discontinued operation, you should present it separately from other continuing operations in your financial statements.

Thus, the readers of your financial statements will be able to see what you put away and what you keep going on in order to generate future profits and cash flows.

More specifically, you should present (IFRS5.33):

- In the statement of comprehensive income: a single amount comprising the total of:

- The post-tax profit or loss of discontinued operations, and

- The post tax gain or loss recognized on the measurement to fair value less costs to sell a or on the disposal of assets or disposal groups.

The analysis of a single amount shall be reported in the notes or in the statement of comprehensive income.

- In the statement of cash flows: the net cash flows attributable to the operating, investing and financing activities of discontinued operations. You can present these disclosures in the notes or in the financial statements themselves.

- In the statement of financial position (IFRS5.38): you shall present a non-current asset or assets of a disposal group classified as held for sale separately from other assets. The same applies for liabilities of a disposal group classified as held for sale.

Please watch the following video with a summary of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations:

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

119 Comments

Leave a Reply

In the notes to the financial statements, should you list all the individual non current assets?

No, only if some of them is material enough to be listed.

if the management decided to go for cost model rather than using fair value model, what would be the accounting treatment.

Dear Silvia,

I have a question with regards to the trading properties.

The trading property has been valued by a third party and in the previous year and has recognized a loss in the profit and loss. when its come to the current year the same Trading property has been valued and shown a gain as per the valuation. In this context, what will be the treatment in the financial statements?

Thanks

hello hope this would be helpful

if you are using ( IAS 40 investment property) directly recognize the current year gain in the statement of profit and loss and in the statement of financial position change it to the new fair value

in which section of the cashflow you present the sale of a building classified as held for sale? will the proceeds go to investing activities? The gain/loss on sale will go to operating activity as non-cash adjustment to the net income?

The ordinary course of the business is NOT to sell buildings.

thank you!

Thank you.

Alvin,

according to IFRS 5.33c, you should disclose the net CF from investing, operating and financing activities related to discontinued operations. So if that building relates to discontinued operations, it is a separate amount within investing activities; if it is only held-for-sale asset without any operation being discontinued, then within investing activities. Best, S.

Hello, I’m from a banking industry. My question is the accounting treatment (initial recognition & subsequence measurement) of a bank purchase a collateral (land/building) from customer so that the customer can use the money to pay off their debt. The bank will resell the land/building within 1 year.

If a subsidiary was purchased with a view to be disposed, can you please advise what needs to be disclosed in the statement of cash flows? Is it the net cash flows attributable to the operating, investing and financing activities?

Dear Georgette,

If a subsidiary was purchased with a view to be disposed of in the near future, the transaction would be considered a discontinued operation, and the results of the subsidiary’s operations would be presented separately in the income statement and the statement of cash flows.

In the statement of cash flows, the cash flows attributable to the discontinued operation would be presented separately from the continuing operations. The net cash flows attributable to the discontinued operation would include the cash received from the sale of the subsidiary, as well as any cash flows related to the operation of the subsidiary during the period prior to its disposal. These cash flows would be classified as operating, investing, or financing activities, depending on the nature of the cash flow.

It is important to note that the disclosure requirements for a discontinued operation can vary depending on the accounting standards applicable to the company. Companies should consult with their accounting advisors and refer to the relevant accounting standards when preparing their financial statements.

If a subsidiary is acquired with the intention of selling it in the near future, the transaction is treated as a discontinued operation and the results of the subsidiary’s operations are presented separately in the income and cash flow statements.

Cash flows attributable to discontinued operations are presented separately from continuing operations in the statement of cash flows. Net cash flows attributable to discontinued operations include cash received from the sale of subsidiaries and cash flows related to the subsidiary’s operations during the period prior to the sale. These cash flows are classified as operating, investing or financing activities depending on the nature of the cash flow.

It is important to note that disclosure requirements for discontinued operations may vary depending on the accounting standards applicable to the company. Companies should consult their accounting advisors and refer to relevant accounting standards when preparing their financial statements.

Please how do you account for the disposal of non-current assets held for sale where the consideration or proceeds is yet to be received?

When you deliver the asset, then you do recognize the revenue from its sale and a receivable.

Investment in shares of company, Which is 55 %, so it is a subsidiary. After many years, as subsidiary not started business, i want to sell the investment in subsidiary as approved by Board/Shareholders on 31/3/2021, and want to recover my money. buyer is found, sale is highly probable and to be completed with in year. Money not received at 31/3/21, it will be recovered 50% on 15/6/21 and balance on 15/12/21, whether i would consolidate as at 31/3/21, or classify held for sale, and on 30/6/21 whether i classify held for sale and consolidate upto 15/6/21, and if classified as held for sale it would not be consolidated?

Dear Silvia,

our company bought major previously abounded factory, with intention to restart the business. It is completely different line of activity from the main Company’s activity. However, the management decided not to enter into the new line, and the factory, together with the equipment will be sold. The management did not actively seek for a buyer during 2020, due to COVID – 19. How to classify abounded factory sold with intention to rebuild the business, and later on concluded not to reorganize the factory, and to sell it. The fair value has been assessed as of 31 December 2020. Thanks

Dear Jani,

The accounting treatment for the abandoned factory will depend on whether it meets the definition of a discontinued operation under IFRS 5 “Non-current Assets Held for Sale and Discontinued Operations”.

According to IFRS 5, a discontinued operation is a component of an entity that has been disposed of or is classified as held for sale and represents a separate major line of business or geographical area of operations, or is part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations.

If the factory meets the criteria for a discontinued operation, it should be classified as such and the results of its operations should be separately presented in the income statement. Any gain or loss on disposal should also be separately disclosed.

If the factory does not meet the criteria for a discontinued operation, it should be accounted for as a non-current asset held for sale, and should be measured at the lower of its carrying amount and fair value less costs to sell. Any impairment losses should be recognized in profit or loss.

Since the management has already decided to sell the factory and has assessed its fair value as of December 31, 2020, it should be accounted for as a non-current asset held for sale. Any changes in fair value subsequent to the date of assessment will not be recognized in the financial statements.

Once the factory is sold, any gain or loss on disposal should be recognized in profit or loss, and the factory should be derecognized from the balance sheet.

Great Website

Asset held for sale can depreciate if still in operation?We are doing the impairment loss instead.

Please reply

Dear Syed,

if an asset that is held for sale continues to be used in operations, it may still be subject to depreciation or amortization until it is sold. In this case, the asset should continue to be accounted for in accordance with the relevant accounting standards until it meets the criteria to be classified as held for sale.

If an asset held for sale is impaired, the impairment loss should be recognized in the income statement and the carrying amount of the asset should be reduced to its fair value less costs to sell. This is consistent with the lower of cost or market principle that applies to assets held for sale.

In BBP, eg 1. A full year Subsidiary met Held For Sale requirements From Oct 1. First 9 months were consolidated and last 3 months reported under IFRS 5 as discontinued.

In eg 2 A Subsidiary was acquired Oct. 1 with a view for resale with requirements met 31 December, the reporting date. The full 3 months were reported under IFRS 5 as discontinued operation. I am confused because under eg 1 discontinuation IFRS 5 took effect from Oct. 1 when requirements were met and under eg 2 requirements were met at 31 Dec but they still discontinued from Oct. 1 using IFRS 5 accounting. Please explain. BPP Chap 13 examples.

Hello, may I kindly recommend looking to the BPP book solutions? I am sure there will be the right explanation 🙂

Dear Silvia,

thank you for your work simply amazing. Related to the topic, I have a question relating to the accounting for other side, when a company has discontinued operation or a disposal group, however instead of selling it company decides to create a separate entity (with same shareholders) and give this assets to that company (demerger of a sort however, the assets/liabilities in a new company were classified as discontinued operations), can you reference me what the accounting in the new entity for this assets/liabilities/equity should be.

Thanks in advance.

if an assets is sold on going concern basis eg running business . is it included under IFRS 5 or not

Hi Silvia,

I have problems on understanding the impairment losses and reversals.

In my understanding, IAS 36 would be ineffective if asset or disposal group has been classified as Asset Held for sale. So, the impairment loss for asset or disposal group that has be classified as Asset held for sale, is the difference between Carrying Amount and FV less cost to sale,right?

How about the other asset that are not within the scope of IFRS 5 such as deferred tax expense and so on? How does the impairment loss is recognized?

Hi Silvia

i have a question regarding how i treat the entries under ifrs 5 when calculating total Carrying Amount

Inventory(1/7/2017) 7 500 000

Inventory(30/6/2018) 5 900 000

Liabilities related to plant-1/7/2017 4 650 000

-30/06/2018 3 480 000

Investments (1/07/2017)(fair value) 15 000 000

(30/06/2018) fair value 18 000 000

Required

Outline the accounting treatment for the group assets in terms of IFRS 5 on 30/06/2018

Hi silvia, I have a questions regarding on the recognition of impairment losses and reversals. Can you please explain in detail?

An impairment loss posses when we have indicator only. when the carring amount grater than the recoverable amount and the indicator should be internal and external. then the carried amount would be there cost added and accumulated dep added to the impaired loss amount. after we deduct the impairment loss in the PPE asset, we test every year to find the reversals amount. the reversals amount should not be grater than the impairment loss .

Dear Selvia

How are you my teacher i just wanna to ask is still there (IFRS – 4 ) as you wright • Contractual rights under insurance contracts as defined in IFRS 4 Insurance Contracts.

After Issuance IFRS – 17 or the IFRS- 17 Still Not Not implemented yet

Hello Madam, If a subsidiary company transfer whole business to its parent company through the Business Transfer agreement then this is called as discounted operation ?. After business transfer subsidiary is not having any business.

Hi

If you sell cars and you sold 8 cars for R80000 each vat inclusive.

Markup is 45% on cost.

What will be the income earned from the sale of vehicles?

Do you deduct the vat inclusive or not

Will the income be R640000?