Example: Construction contracts under IFRS 15

Ever since the new revenue standard IFRS 15 Revenue from Contracts with Customers was issued, I get one and the same question:

What happened to construction contracts?

They were guided by IAS 11 Construction Contracts, but you might well know that after 1 January 2018, IAS 11 became superseded – it does NOT apply anymore.

Under the new IFRS 15, construction contract is treated exactly the same way as any other contract with customers.

I know I know.

Sometimes it’s hard to apply and imagine what it looks like.

Therefore in today’s article, I would like to show you HOW you should account for construction contracts under IFRS 15.

Plus, I will illustrate everything on an example with journal entries and calculations.

What do the rules say?

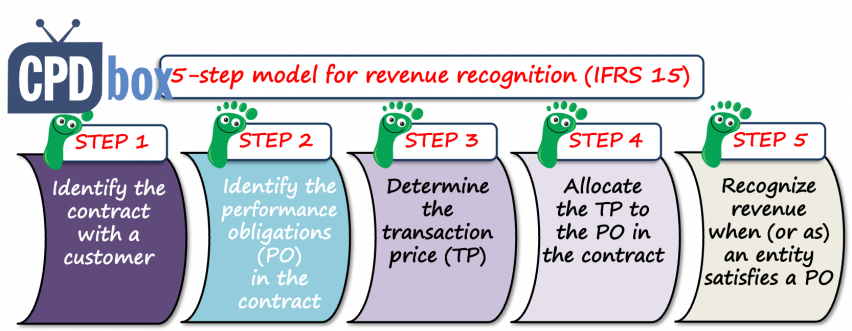

IFRS 15 prescribers the 5-step model for the revenue recognition.

You can also check out my IFRS Kit with detailed video tutorials about IFRS 15.

To sum up, here are the 5 steps:

- Identify contract with the customer;

- Identify the performance obligations in the contract;

- Determine the transaction price;

- Allocate the transaction price to the performance obligations in the contract;

- Recognize revenue when (or as) an entity satisfy a performance obligation.

If you enter into the construction contracts with your customers and you previously applied IAS 11, then you need to follow exactly these 5 steps under IFRS 15.

Let me show you straight on an example.

Example: Construction contract under IFRS 15

Construction company ABC signs a contract in June 20X1 to refurbish a building and install new windows with window blinds (let’s call it “windows”). Total contract price is CU 12 million.

Total expected contract costs are:

- CU 6 mil. for windows (purchased from external suppliers);

- CU 4 mil. for labor, materials and other costs related to the project.

As of 31 December 20X1:

- ABC handed over windows to the client, although the installation has not been completed. However, the client obtained control of windows.

- Other costs incurred to 31 December were CU 1 mil.

Just before the year-end, the client paid the first progress payment of CU 8 mil.

How should ABC account for this contract as of 31 December 20X1 in line with IFRS 15?

Let’s follow the 5 steps for the revenue recognition.

Step 1: Identify the contract with a customer

It is very clear now, we have the explicit contractual agreement between ABC and a customer.

Step 2: Identify the performance obligations in the contract

You need to identify not only individual goods and services promised in the contract, but also determine whether they are distinct or not.

Again, I will not go into theory explanations here, you can learn about distinct/not distinct either in my article here or inside the IFRS Kit.

If the goods and services are not distinct, they can’t be provided one without the other one (this is very simplified explanation) and thus they must be treated as ONE single performance obligation.

According to ABC’s assessment, the reparation services, windows and installation of windows are ONE single performance obligation.

Most construction contracts will contain just ONE performance obligation, because the contract would be to build or construct something for the customer and is negotiated as a whole package where a customer has no choice than to get the full package from the supplier.

Sometimes it’s not true and you will have TWO or more performance obligations there.

In this case you must adjust your accounting accordingly as explained below.

Step 3: Determine the transaction price

The transaction price in ABC’s contract is CU 12 million.

This is clear, but in reality, you can have some variability involved, like progress or performance bonuses.

You should take these estimates into account, too based on their probability.

Step 4: Allocate the transaction price to the individual performance obligations

This is very easy here, because as ABC assessed in the step 2, there is just ONE single performance obligation and thus the whole transaction price is allocated to this ONE obligation.

If there would had been more than one performance obligations, then ABC would need to allocate the transaction price to them based on their relative stand-alone selling prices.

You can revise the short example in this article to make it totally clear.

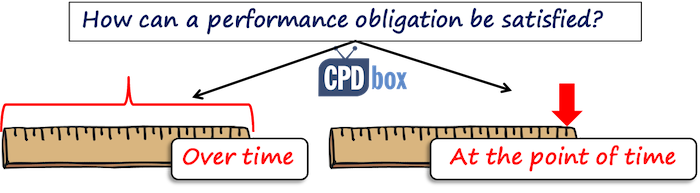

Step 5: Recognize revenue when (or as) the entity satisfies a performance obligation

You should remember that the performance obligation can be satisfied either:

- At the point of time; or

- Over time.

The standard IFRS 15 lists a few criteria when a performance obligation is satisfied over time:

- Customer simultaneously receives and consumes as the entity performs;

- Customer controls the asset enhanced or created by the entity;

- Entity does NOT create an asset with an alternative use and has an enforceable right to payment for performance completed to date.

If you meet just one of these criteria, then the performance obligation is satisfied over time.

In most construction contracts, the performance obligations are satisfied over time and NOT at the point of time (although exceptions might exist).

In this case, you need to recognize revenue based on the progress towards completion.

How to measure progress towards completion?

You can use either input or output methods to measure the progress towards completion.

ABC uses input method, i.e. based on costs incurred to date.

Also, let me warn you about one significant factor specific especially for construction contracts:

There may be no direct relationship between your inputs and the transfer of control of goods or services to a customer.

Therefore, you should exclude the effects of any inputs from input method that do not depict your performance in transferring control of goods or services to the customer (par. B19 of IFRS 15).

Translated to human language and applied to this example:

ABC believes that costs of windows are significant item within total costs and including these costs to measure the progress to completion would not be appropriate, because it would certainly overstate ABC’s performance.

The reason is that the windows are purchased from the third party and the transfer of windows to the customer has no direct relationship with the other ABC’s work.

Therefore, progress towards completion will be measured excluding the cost of windows.

Carefully, because you should apply the resulting percentage of completion to the revenues excluding windows, too – just for the consistency!

Let’s measure the progress towards completion:

- Total costs excluding windows: CU 4 mil.

- Total incurred costs to date excluding windows: CU 1 mil.

- Progress to completion: CU 1/CU 4 = 25%

- Total contract revenue excluding windows: CU 6 mil. (CU 12 – CU 6)

- Total revenue to 31 December 20X1 excluding windows: CU 6 mil. x 25% = CU 1.5 mil.

Journal entries at 31 December 20X1

As we excluded windows from measuring progress towards completion, we will draft the journal entries separately for windows and for the remaining services.

Windows:

As ABC handed over windows and excluded them from measurement of progress towards completion due to potential overstatement, the revenue from sale of windows is recognized at the time of their delivery.

Purchase of windows by ABC (at the time of delivery from the supplier):

- Debit Inventories: CU 6 mil.

- Credit Suppliers: CU 6 mil.

ABC recognizes the revenue for windows at zero profit margin (equal to their cost – in line with par. B19(b) of IFRS 15):

- Debit Contract Asset: CU 6 mil.

- Credit Revenue from construction project***: CU 6 mil.

***Not the revenue from sale of windows – remember, the whole project is one performance obligation and we recognize the revenue under 1 caption in this case.

Cost of windows:

- Debit Costs of construction in profit or loss: CU 6 mil.

- Credit Inventories: CU 6 mil.

The remaining cost/revenues:

Labor costs, materials, etc. to complete the contracts are accounted for as contract costs (at the time when they are actually incurred):

- Costs to paint the building:

- Debit Contract costs (asset in balance sheet);

- Credit Employees (or suppliers or whatever is relevant)

- Use of paints:

- Debit Contract costs (asset in balance sheet)

- Credit Inventories

At 31 December 20X1, ABC needs to amortize the contract costs based on progress towards completion.

As the progress is measured by input method (incurred costs), all costs incurred to date are amortized.

However if different method is used to measure the progress to completion, then the company can amortize the cost based on the progress percentage.

In this case, at 31 December 20X1:

- Debit Cost of construction in profit or loss: CU 1 mil.

- Credit Contract costs: CU 1 mil.

Let’s recognize the revenue from “remaining” services (all except for windows).

We measured these revenues at CU 1.5 mil. using the progress towards completion (please see above).

Journal entry is:

- Debit Contract asset: CU 1.5 mil.

- Credit Revenue from construction project: CU 1.5 mil.

Finally, we need to account for the progress payment of CU 8 mil. made by the customer at the year-end:

- Debit Trade receivables (bank account, cash…): CU 8 mil.

- Credit Contract assets: 8 mil.

Let’s check the contract asset now. Its balance at 31 December 20X1 is:

- Contract asset that arose at revenue recognition (6+1.5): CU 7.5 mil.

- Less progress payment by the customer: CU 8 mil.

- The balance: CU -0.5 mil..

As the contract asset is negative at the end of 31 December 20X1, it became a contract liability and it should be presented within liabilities in the statement of financial position.

I personally prefer to see contract liabilities at the year-end, not contract assets, because:

- We have no credit risk as we have no performance completed to date which is not paid by the customer, and

- We don’t have to calculate expected credit loss and measure the impairment on contract assets – hurray!

Finally…

This is basically the method you should follow when accounting for your construction contracts.

I tried to make this simple as possible, but I can’t cover every single situation here.

If you have any questions, please ask them in the comments or you can even consider subscribing to our IFRS Helpline where I and my amazing team answer to your very specific question, issues, help you apply IFRS or even implemented for the first time. Just write me an e-mail if you’d like to get more information.

Thanks!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

126 Comments

Leave a Reply

Hi Silvia, can you please provide output method illustration?

Kindly advise how to measure the cost of sale if using the output method?

Should we recognise the cost of sale based on actual cost incurred? or we use % of completion based on output % x budgeted cost?

Thank you.

What happens to the contract cost CU 1 (Cr balance) from the double entry of Cost of construction dr 1 and contract cost cr 1. Kindly explain to me

This is a great resource for anyone working with construction contracts! The breakdown of the 5-step model with the example using the construction company ABC is very clear and easy to follow.

It would be interesting to see a more complex example, perhaps one where the performance obligations are not distinct. For instance, a construction contract that includes both building the structure and installing pre-designed cabinets. Do you have any resources that explore the allocation of the transaction price when dealing with less clear-cut performance obligations?

In my company, work in progress is accounted as debiting WIP a/c and Crediting the Contract cost, they compute the value of uncertified work and reduce the margin to arrive at cost and that is reduced from the contract cost, is it correct ?

Also for some projects, they are accounting as crediting revenue and debiting the WIP for the uncertified work. i think this is the correct method. which one is correct?

Hi Sylvia

Thank you for your explanation.

One question: as you explained, at the end of the project we would at all account only 6mln revenues but 10mln costs? Is it correct? Regards, Olga

What are the journal entries for retention sum? Would the contract asset also contains retention sum?

Please see the short example with journal entries here, I have answered that some time ago. I hope it helps!

Hi Silvia,

I am from a shipbuilding company; one thing I am not clear regarding revenue recognition in the construction contract. As per IFRS 15.35(2) states about control transfer to recognize revenue, however, to build a ship it requires 2 to 3 years. At the year end, I have to measure % of completion and according to this revenue is to be recognized; but what about control, here control is not transferred. Based on which ground, we are recognizing revene?

If I may ask what would be the accounting treatment if the construction contract has been cancelled and the cost is partly reimbursed?

That depends on the stage at which the contract was cancelled and on the specifics of that contract, so I really cannot say based on this info.

After 2 days of searching internet for practical information regarding income recognition from contracts this is the most helpful article.

Thank you

I thank you, I am glad to help 🙂

HI SILVIA

in this example, we exclude value of windows. Assume material supplied but not installed in the end of financial year .cost of material = revenue with zero profit .what about other sales related costs( indirect costs like bank charges. Letter of guarantee charges,etc specific to this project) .In that year it will show loss due to under statement of revenue

How to deal with those expenses.i think we include only direct costs for performance measurement.please advise

Dear Silvia,

Thank you for the article, very clear, i want to get your feedback regarding our case, we are a manufacturing company, we have stated to apply IFRS15 and for that we are moving the stock variations of harnesses to revenues, and the Finished goods inventories to contractual assets, and we are adding an uplift calculated based on a a group definition. I’m wondering if it’ correct and also if there is any specific method to calculate the uplift or to check if it’s the correct one.

Thank you

Dear silvia

Can I record the revenue with my completion percentage without issuing a sales invoice, knowing that a sales invoice will be issued at the end of the period

Assuming that the entire process will be completed within three years

And if I do that when I issue the invoice after three years, what will I record in lieu of revenue?

Thank you in advance

Hi Sylvia,

Can you please explain shortly catch up accounting related to IFRS 15 construction contract, if possible with example..

I am puzzled now, because I believed this whole article is about IFRS 15 Construction contracts with example.

Hi Sylvia,

If customer does not take the position of the constructed asset, though paid full, then how the construction entity and the buyer will account for this?

Hi Sylvia

Need an opinion on the following

A promoter is constructing villas and the customer has already given deposits for the villas.

How to recognise revenue

Hi Navin, it depends on how the rights of the customer are formulated in the contract. It could be both ways, at the point of time (at the hand-over day) or over time (according to the progress towards completion), depending on the contract.

As per your Article , can we amortize the contract cost..? because these cost seems already incurred, specially labor… At the same time , shouldn’t we consider these cost in computing percentage of completion (e. g cost to paint, paint issued to site). Since we recognize revenue over the period , it is bit confusing recognizing these type of cost as an assets and being amortized over the period of time..?

Hello Sylvia, under the situation of a construction contract (using the percentage of completion method or revenue recognised over time) that encounters a situation where the percentage of cumulative revenue to be recognised in a subsequent year is lower than the previous year, how should the revenue/contract asset be recognised, if at all?

Hi Silvia, What if a deposit is received from the customer? How would it affect the journal entries? I was thinking the following (using Unearned Revenue account) but it may result in Contract Asset being negative even upon completion of the contract and full payment by customer as a smaller amount of revenue is debited to Contract Asset while the same amount of costs is credited to Contract Asset. Could you please advise?

Upon receipt of deposit:

DR Bank

CR Unearned Revenue

Upon recognition of revenue:

DR Unearned Revenue

DR Contract Asset (remaining)

CR Contract Revenue

Hi Jo, if you receive any amounts prior to satisfying performance obligations, that’s a contract liability, not a contract asset 😉 Otherwise, not a bad thinking 🙂

Hi Silvia

Am I correct in saying construction contract revenue can only be recognised over time according to the third criteria when it is written in the contract invoices can be raised at certain milestones i.e. enforceable? Does this include where work stops and the entity is entitled for costs incurred to be covered?

Many thanks

Hi Silvia. Do we capitalize the short term hire of construction vehicles for a project ?

If you hired them just for this project, then yes, this is directly attributable and incremental.

Hi Silvia, I have one question here regarding the contract cost. Let’s said the Method used to measure the progress toward completion is based on “Output” instead of Input method and if the contract cost shall be amortized based on POC instead of cost incurred to-date? Sometime very confusing as I though construction cost shall be recognised once incurred..,.

Hello Sylvia, thank you for the explanation. I have one question. In the old IAS 11 based on percentage of completion (POC), we had something called underbilling and overbilling. Is this what has been replaced by contract asset and liabilities? Under billing/overbilling is when you compare your expected revenue based on your margin expectation as against actual progress billing to your client. Here I am referring to a construction company with 3 years road project. Thanks for your help.

Hi Fredrick, yes, we could say simplistically that “overbilling” leads to contract liabilities and “underbilling” to contract assets.

Great information, cover all aspects

On 31 December 20X1, ABC needs to amortize the contract costs based on progress towards completion.

As the progress is measured by the input method (incurred costs), all costs incurred to date are amortized.

However if a different method is used to measure the progress to completion, then the company can amortize the cost based on the progress percentage.

Please give an example of a different method. Appreciate your dedication

Hi Silvia, many thanks for the above explanations and making IFRS easy to understand and implement the concepts. I have one question relating to recognition of losses in construction/service contracts known at the time of signing the contracts.

A company signs a services sales order in loss due to some estimation errors known at the time of signing the contract. The execution is spread over two accounting periods. How much of loss should be recognized by end of first accounting year ? The full known loss being conservative or proportionate to progress of project ? Many Thanks

Hi Silvia- As a commercial building owner, when I receive a large (half a million dollars) construction contract to do some interior improvements, do I record the full contract amount as a liability or do I just record the progress billings as I receive them? In other words, does the $500k need to show on the Balance Sheet as a liability even before the work begins?

Dear Silvia,

Thank you for this article.

I have a question and I would appreciate your help.

A company develops software and recognizes revenue over-time. It uses the input method (cost-to cost) to measure progress toward completion. The costumer has a certain period of time to sign off the acceptance. In such case, when are the costs incurred recognized in P/L? If I understand correctly, according to IFRS 15.98 (c ) they are expensed as incurred since they relate to a partially satisfied performance obligation. So, in the case that the customer acceptance is signed off in the next period, the revenue and costs would not match. Could you please confirm whether my understanding is correct ?

Mary,

that paragraph relates to a different situation. Still, you should use progress to completion method to recognize revenue (and expenses). S.

Hi Silvia,

Thank you for your quick reply.

Just to clarify, shall in this case both revenue and expenses be recognised in the same period?

I was looking at the Agenda Decision, ‘IFRS 15 Revenue from Contracts with Customers—Costs to fulfil a contract’ from June 2019 and my undersatnding is that the costs discussed in the agenda are similar to my case and that such costs relate to past performance and shall be expensed as incurred. So, if acceptance is signed off in the next period by the customer, revenue and costs would not match.

I would really appreciate your comment on this.

Hi Mary, if that past performance has already been recognized in the revenues, then yes, the costs shall be expensed. Past performance shall be understood as something you have already performed in the past (thus implicitely you have already recognized revenues for that). So it is not “past” in a sense that you are still working on it and the client has not accepted.

Also, it depends on whether you recognize revenue over time or at the point of time. If over time based on progress towards completion, then the control of the goods/services transfers to the client over time regardless the exact time of acceptance. However, if control transfers at the point of time and acceptance signature is that point of time, then the costs incurred to provide that good/service transferred at that point of time do not relate to past performance, but the performance not yet accepted. I hope it is a bit clearer.

Hi Silvia,

Thank you very much for clarfying this.

Hi Slyvia,

I need some clarification, I recently started working with this company that acts a forwarding and clearing agent so when they invoice clients, they generally include the shipping and handling fees along with the duties paid on behalf of their customers. My question, how should those duties be treated in the accounts since it is not exactly revenue. Thanks and I await your explanation.

Dear Silvia,

If we were to change the purchase of the windows to a pay-when-paid transaction, and the vendor invoiced the windows but it was unpaid at year end, would the window payable be reported as accounts payable or a contract liability?

As soon as there’s an invoice from the supplier, it is your payable. Having that said – contract liability has NOTHING to do with the suppliers. It all relates to the customers. For example, customer pays you up front some advance payment of 10 000 and you haven’t even started the project work for this customer – hence 10 000 is your contract liability.

Dear Silvia,

What do we do exactly with the contract that is loss-making? Does IAS 37 guidance of onerous contracts apply to such contracts? If it does, how, can you please give an example. Thank you!

How we present contract costs in the financial position current or non current???

Based on the expected time of their settlement.

Hi Silvia

Thank you for your amazing explanation as usual, my question regading the booking of cash or receivables when invoiced to the client, as you have mentioned in the example above, Dr. Trade receivables, Cr. Contract assets. but i thing this is different from the entry in your excel sheet#8 of IFRS16, as you have debited A/R, Credited Contract liability.

can we say both entries have the same effect as decreasing assets have the same effect of creating liability.

But in the example in the Excel sheet, i think there some are entries missing, whis is the booking of contract cost ( Assets ) ? Am i right ?

Thank you