Accounting for CAPEX threshold and its change under IFRS

Many companies apply so-called CAPEX threshold to decide which assets to capitalize and which assets to expense in profit or loss, based on their acquisition costs.

I received many questions related to CAPEX threshold, so I selected one of them because it is the most complex one:

“We have a CAPEX threshold policy where we capitalize all assets with cost higher than the threshold.

Let’s say that the threshold is CU 1 000. What if we buy lots of assets at CU 700 each?

It does not seem OK to pass them in profit or loss because their total value is more than CU 1 000.

Also, how to set the threshold – any advice?

What happens if a company revises its capitalization threshold from CU 1 000 to CU 1 500 will be accounted for as change in accounting policy and will be applied retrospectively?”

IFRS Answer: Materiality and aggregation

It all has something to do with materiality and aggregation.

You need to set up your materiality level first.

What is material?

The standard IAS 1 Presentation of Financial Statements specifies that material is anything that could either individually or collectively influence the economic decisions that users make on the basis of the financial statements.

So it’s certain significance or importance.

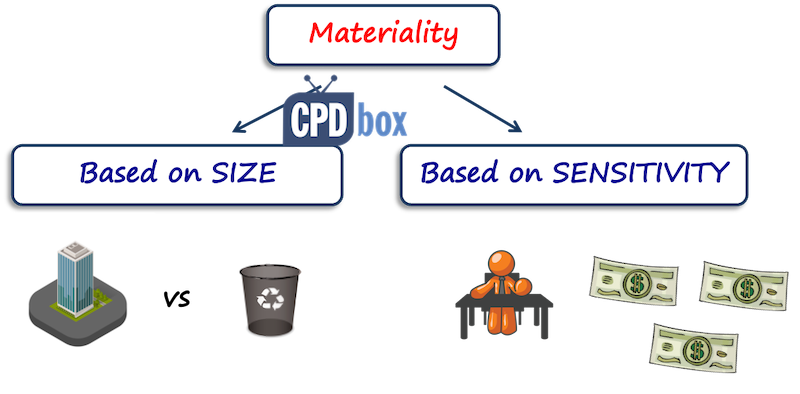

An item can be important due to 2 basic factors:

- Its size – the purchase of the whole admin building will probably be material for a medium-sized company, but not the purchase of waste paper bin, and

- Its sensitivity – some items can be material not due to their size, but due to their sensitivity because they can have an impact on how other people perceive the company.

Typical example are bonuses to management.

They might not be significant – USD 1 or 2 mil. paid to CEO of some big multi-billion or gazzilion corporation is probably not material due to the size, but people always watch out on how the companies remunerate their managers and whether the shareholders are not in conflict with management.

Now, we will focus on the size.

Assessing the materiality

Materiality is something that must be assessed by each company individually.

The reason is that it depends on the company’s size, nature of operations, magnitude of individual information and its significance for financial statements etc.

Materiality is very judgmental and yes, each entity must determine it, there is no exact and explicit process of setting the materiality.

However, in September 2017, IFRS Foundation issued the IFRS Practice Statement n.2 titled Making Materiality Judgments.

This statement describes the process of setting your materiality levels, it has 4 steps – identify, assess, organize and review, and you can actually download the full practice statement for free at ifrs.org.

Individual or aggregate?

OK, so you set up your materiality.

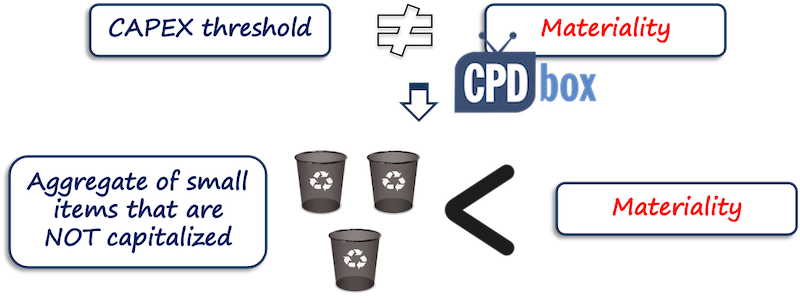

The capex threshold is NOT a materiality, but it is very closely related to it and derived from it.

The capex threshold should be set in a way that the total amount of items expensed in profit or loss is not material.

So if the aggregate of small items not capitalized due to being lower than the threshold is lower than the materiality, then your threshold is set correctly.

Let’s say you set the threshold of CU 1 000.

Thus, everything expenditure over CU 1 000 gets capitalized as it is significant, and everything below CU 1 000 is expensed in profit or loss.

Fair enough.

Now, what about the situation when you buy 5 assets, CU 700 each?

It means that you made a purchase of CU 3 500.

Individually, it is not material, because it’s below your materiality level or capex threshold.

But, in aggregate, it is material.

The standard IAS 16 Property, Plant and Equipment describes that in paragraph 9.

It says that it may be appropriate to aggregate individually insignificant items, such as tools or molds, and apply the recognition criteria to the aggregate value.

If the aggregate value is lower than your threshold, then expense in it profit or loss.

Revising your capex threshold

What happens when you actually change the threshold from CU 1 000 to CU 1 500?

How should you apply that change?

If you have set the thresholds, you should revise them each reporting period – that is at least once per year.

You should really look at whether the current amount is still immaterial, not affecting your users.

Should you reflect the change in materiality – or the change in capex threshold in this case retrospectively?

Yes, sometimes.

It depends on whether your capex threshold increases or decreases:

When your capex threshold decreases…

Imagine that some asset meets the definition and recognition criteria for property, plant and equipment under IAS 16, but you do not recognize it as an asset because its cost is lower than your threshold.

What actually happened?

You made an immaterial error, isn’t it?

Let’s say that your capex threshold is CU 1 000 and you bought a bookshelf for CU 800.

The bookshelf is a property plant and equipment because you plan to use it to store your office files for more than one year.

So you should capitalize it and depreciate it as an asset if you want to be 100% correct.

But, it is not material, so you can expense it. You just made an immaterial error in fact.

The next year your company shrinks for some reason, profitability goes down and smaller items become material.

You revise your capex threshold from CU 1 000 to CU 700.

And, what was immaterial error last year, becomes material error. Sometimes it’s not the case, but you should check that.

You should make a correction of this material error under IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors – that is retrospectively.

The IFRS Practice statement that I mentioned also asks for it in the paragraph 80.

When your capex threshold increases…

When you increase the capex threshold, then material items become immaterial and thus there’s no cumulative error from the previous periods.

So no, if you revise the threshold upwards, there’s no need to correct.

Here’s the video summing up the issue:

Any comments or questions? Please use the form below to ask!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

20 Comments

Leave a Reply

article is useful

Hi Silvia,

Thanks a lot for your useful article. I have the question, lets say our CAPEX threshold policy is 5,000 CU. In the same accounting period, we are acquiring small value items each 1,000 CU. In this case, we are considering aggregation value to recognize PPE under IAS 16. In the same accounting period, we are again acquiring same only one item. If we are directly charging to P&L, we will unable to control the asset. Lets say, while we go for asset verification or counting, it will give the confusion to us which items needs to consider under PPE. So, could you please clarify in terms of controlling and proper treatment under IAS 16.

Hi Alifar,

this is exactly the process YOU have to set in your accounting manual.

So, if you acquire small items with aggregate value above threshold, I said in the video what to do: it would be appropriate to capitalize it and keep a good track. If you acquire additional item, just treat it as subsequent cost and add it to PPE. For example, take library. Each book is certainly below any threshold, but in aggregate they are massive. And, they need to keep record on each book.

How to control it? It would be good to stick unique number to each item if possible. QR codes or bar codes work extremely well. Not sure though if this is what you were asking me. S.

Hi Silvia,

Thanks for your time and reply. Yes. This is what exactly I asked.

Hi, Silvia, thank you for this aticle.

My question is: CAPEX thresholds are more related to the acquisition cost of PPE. Change of the threshold from CU 1 000 to CU 1 500 – is change accounting policy? Can we change accounting policy in the middle of the financial year? Thank you very much for the help

Hi, Silvia, thank you for this issue, I found it very useful.

My question is: How to apply threshold policy in connection to the revaluation or impairment of PPE?

For example: We have an engine recognized initially at 10.000 CU with 7.000 CU depreciation, i.e. 3,000 CU carrying amount. Its fair value is determined at 1.000 CU. Our CAPEX threshold is 2.000 CU. The accumulated depreciation is eliminated against the gross carrying amount of the engine. The decrease is recognized in profit or loss. As a result the gross carrying amount of the engine becomes 1.000 CU, under the CAPEX threshold. Should the engine be derecognized?

Thank you in advance!

Hi Svetlana, these CAPEX thresholds are more related to the acquisition cost of PPE, not the carrying amount after depreciation and impairment:) S.

Hi Silvia, I have particular question relating to CAPEX threshold increase.

For example, previously CAPEX threshold was 5000 CU and not it has become 10,000 CU.

Q1 – Is it consider as change in accounting policy? If yes, how should we deal with it?

Q2 – How to deal with the assets which are already capitalized in the past valuing between 5,000 CU and 10,000 CU and not yet reached to zero value? Do we have to write it off? If not then how should we deal with it?

Appreciate your response.

Hi Malav, please read the above article again, I wrote what happens when you revise thresholds. Thank you!

Thanks. I read it. However, it is still not clear to me.

Please confirm that already capitalized item below threshold value, we need to continue depreciation.

Good day Silvia,

I agree with Malav that it is not really clear on the article in addressing his two question. I also have the same two question that I would appreciate your clarity.

OK, copying from the article: “When your capex threshold increases…

When you increase the capex threshold, then material items become immaterial and thus there’s no cumulative error from the previous periods.

So no, if you revise the threshold upwards, there’s no need to correct.” Which part is not understandable, please?

Ok to be more specific to my query, we have a number of asset with small values on our asset register. Now, we want to remove them by increasing the capitalization threshold value to write them off the register. Is that allowed or there is another way to write off small value/immaterial items that are still in use?

Hi Silvia,

I have a question on the topic of PPE. Does IFRS addresses the accounting for restricted donations used to acquire PPE. I know that IAS 20 addresses Government grants and allows to apply the government Grant to the Cost of PPE and then apply the amortization to the remaining balance. Can this accounting treatment be used for donations also. In other words can we apply donations as a credit to the PPE cost and then calculate the depreciation on the balance?

Hi Nevila, I am not sure what donations you mean. Can you please specify?

HELLO I CAN NOT UNDERSTAND TERM deffered tax liabilty and asset and how to arise DTL AND DTA PLEASE TELL ME ABOUT THESE TERM WITH EXAMPLE YOUR ATICALE GIVEN AEXAMPLE BUT I DID NOT UNDERSTAND

Silvia, thanks a lot for the article post.Much thanks again. Fantastic.

Thank you

Dear Silvia, Materiality is very subjective and judgmental; there seems to be no underlying principle. It looks like a tool in the hands of corporates to tweak it according to their fancy. For eg: in the scenario of low profitability one tends to make a correction and decrease the threshold so that more items are capitalized and the impact to the Profit and Loss is minimized. The larger question is why cannot the principle of property, plant and equipment be applied in simpliciter; meaning: where the economic useful life is more than one year then it should be capitalized irrespective of the value it carries and hence would be part of the Fixed Assets Register which would also enable it to be physically controlled and there will no question of judgmental application of principles. Where a component forms part of the fixed asset, then of course, we apply the principle of economic life being different from that of the parent and value being substantial in relation to the value of the parent as the qualifying criterion for capitalization. Please let me know

Hi Venkat, I agree – all assets with useful life>1 year (+ used for PPE purposes) should be capitalized and yes, if you have thresholds, you are making “immaterial errors” in fact. But materiality and threshold should be set in such a way so that the impact on profit or loss of capitalizing/not capitalizing is immaterial – that’s the point of it (and of this short article).