IFRS 3: A Business or an Asset?

Last update: August 2023

Did you note that with the globalizing world, the number of large entities decreases and their size increases?

Just as an example – 20 years ago, there were about 50 large media companies in the USA, controlling US entertainment industry.

I mean film studios, TV stations and similar companies.

These days, there are just 6 of them. SIX.

What happened to the other 44? Did they disappear?

No!

Instead, they were acquired by larger companies.

This trend continues and will only flourish in the light of the economic crisis caused by COVID-19.

I bet that we will see even more large acquisitions in the future, not only in the entertainment industry (and let me guess that they will be very cheap but that’s another story).

However, what I also believe is that we will see more acquisitions focusing on strategic assets rather than acquisitions of full businesses.

Why?

Well, because if the owner is in a cash-flow problem, she might be forced to sell just the most attractive parts of her business for the lower price and on the other hand, the buyer can get good assets at a bargain price.

Now the question is:

What is the investor getting?

Is she buying a full business or a group of assets (or a single asset)?

Assets vs. business: Why does it matter?

Simple answer: Accounting method:

- If you acquire the full business, then you need to apply the acquisition method of accounting and full consolidation.

- If you acquire assets, then you do not consolidate, but you simply recognize assets (and possible liabilities) in your financial statements.

The implications are obvious, not only due to differences in the accounting method itself, but the method can have a direct impact on the profitability.

For example, think of goodwill.

If you acquire full business, it is likely you will have some goodwill that you need to test for impairment each year and not amortize.

If you acquire assets, you have no goodwill and instead, it is either recognized somewhere among assets (not exceeding their fair values) or as some 1-day loss depending on the circumstances.

In the long-term perspective, this affects depreciation and amortization charges, impairment losses, etc.

You get the point.

IFRS 3: Definition of business

In 2018, IFRS 3 has been amended with regard to definition of business.

The new definition applies to all acquisitions made after 1 January 2020.

According to IFRS 3 (Appendix A), the business is an integrated set of activities and assets that is capable of being conducted and managed for the purpose of:

- providing goods or services to customers;

- generating investment income; or

- generating other income from ordinary activities.

Elements of business

IFRS 3 also sets that any business must contains three elements:

- Input: this is a resource (e.g. items of PPE, intangible assets, etc.) that can contribute to creation of outputs;

- Process: something that you apply to input and as a result, it can contribute to creation of outputs, for example processes, methods, etc.;

- Output: the result of process applied to inputs, for example goods or services provided to customers, and other.

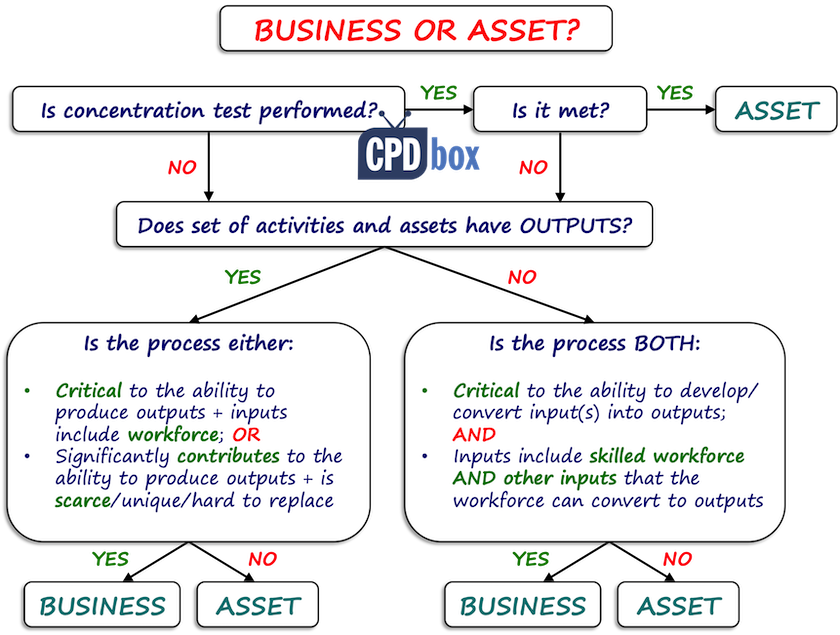

How to assess: Business vs. assets

Before we start assessing whether the acquired activities are a business or a group of assets, we need to make this clear:

Under the new amendment, the business does NOT necessarily have to produce outputs.

Yes, typically it does, but the business can include as a minimum an input and a substantive process.

“Substantive” is an important word here, because if you do have only inputs and minor process, then it is NOT a business, but asset(s).

In fact, we need to assess whether the process involved is substantive – that’s perhaps the main focus of the assessment “business vs. asset”.

When you assess whether there are inputs and substantive process, first you need to see whether the business has outputs or not.

I don’t want to go into too many details here, because paragraph B12 of IFRS 3 provides the full guidance on assessing whether your processes are substantive.

Basically, the process is substantive when it is critical or significantly contributes to the outputs (or at least to the ability to create outputs).

Moreover, when it does not have outputs, then inputs should include an organized workforce AND other inputs that the workforce can develop or convert into outputs.

That’s very simplified and please see the scheme below the concentration test to revise the specific conditions.

Concentration test

Instead of assessing whether you have inputs, substantive process and all other features of business, IFRS 3 introduced new simplification option for you:

Concentration of fair value test.

It is OPTIONAL. You can use it, but you don’t have to.

The principal question in this test is:

Is substantially all of the fair value of the GROSS assets concentrated in a single identifiable asset or group of similar identifiable assets?

- If YES, then it is NOT a business. Work done.

- If NOT, then you can’t really make a conclusion and have no choice but assess inputs, processes, outputs and other features of business as I shortly described above.

Let me make a few remarks to the concentration test:

- Assess GROSS assets, not net assets. The reason is that liabilities (like loans, payables) are not really relevant to assessing whether you are acquiring a business or not.

- Ignore cash and cash equivalents, deferred taxes and goodwill.

- In the calculation of FV of gross assets, include any consideration transferred (plus FV of NCI and previously held interest) IN EXCESS of FV of net assets acquired.

- Similar assets have similar risk characteristics. Consider their nature and risks.

- Assets that are NOT similar are: tangible/intangible; different classes of tangible assets; different classes of intangibles; financial/non-financial; different classes of financial assets, assets with different risk characteristics.

- If the assets are attached and cannot be separated without significant cost, then they are considered a single asset.

The process of assessing whether we deal with the business or assets can be summarized in the following scheme:

Example: Is it business or assets?

Let’s say that ABC, large clothing company, wants to expand to the new location.

During its research it discovers an old factory with infrastructure owned by the local company. Current owner discontinued the production recently.

Currently, there are only a few people working in the factory on the closing works.

ABC decides to buy the factory, but the owner agrees to sell it only with all its liabilities and assets in entirety.

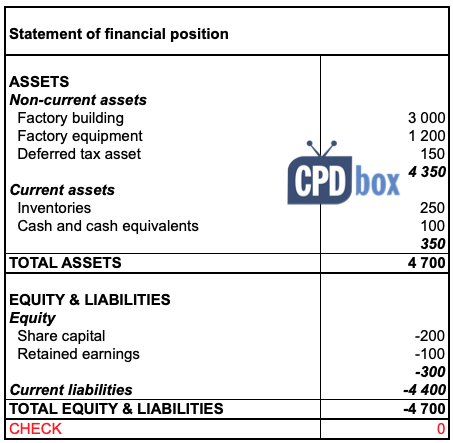

The balance sheet of the factory is as follows:

Fair value of the factory building is CU 3 100. All other assets in factory’s balance sheet are stated at fair values. ABC pays CU 500 for the factory in its entirety.

Let’s assess whether ABC acquired a business or not.

First, let’s perform a concentration test.

We need to calculate fair value of gross assets.

There are two ways of calculating it:

1. Add up gross assets (and excess of consideration paid over FV of net assets):

- FV of a building: CU 3 100; plus

- FV of factory equipment: CU 1 200; plus

- FV of inventories of CU 250; plus

- FV of + consideration paid by ABC: CU 500; less

- FV of net assets acquired: CU 300 (being the equity) plus CU 100 (being FV of building of 3 100 less book value of building of 3 000) = CU 400

- Total: CU 4 650

Remember – you ignore cash and deferred taxes (and goodwill, but there is none).

2. Adjusting liabilities and consideration paid:

- Consideration paid: CU 500; PLUS

- FV of liabilities: CU 4 400; LESS

- Cash acquired: CU 100; LESS

- Deferred tax asset acquired: CU 150

- Total: CU 4 650

OK, so the fair value of gross assets acquired is CU 4 650; and it is mainly concentrated in building and equipment.

However – factory building and equipment are NOT similar assets, because they represent different classes of property, plant and equipment.

The question is whether the equipment can be removed from the factory without significant cost. If not, then the factory and its equipment would be considered a single asset for the purpose of this test and the concentration test would be met.

Let’s assume this is not the case.

As a result, the concentration test is NOT met, the fair value is NOT concentrated in a single asset (or group of similar assets) and as a result, ABC must assess inputs, processes and outputs in order to conclude whether the acquired activities and property are a business or not.

First of all, does the set of activities and assets have output?

No, it does not, because the factory has been recently closed.

Therefore, if it does not have an output, we need to see whether there is a substantive process present.

There is a workforce (a few employees working on the closing of factory), but there are no other inputs that workforce develops or converts into output.

The workforce there only works on the closure.

Thus ABC can conclude that it acquired assets, not a business (no consolidation, but the asset acquisition).

Further reading and lecture

You can learn how to account for acquisition of a subsidiary that is NOT a business, just assets, here. This article contains a step-by-step video in its end.

Please if you have something to say, leave a comment below this article. Thanks!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

17 Comments

Leave a Reply

Thank you for simplifying complex IFRSs

Thanks really worth it!

Hello Sylvia

My company A through its fully owned subsidiary company B established a fully owned subsidiary X. The paid up capital of Company X was US$ 5K and the shares were held by one of the employee of Company B (nominee)

Company X then made a deal with another existing company Y whereby the company Y will transfer its equipment and employees to company X.

Company X will pay US$ 1mn to company Y and 45% of its own (X) equity. company Y will discontinue its operations after the transfer. The employee will transfer the shares of Company X to Company B (55%) and Company Y shareholders (45%) on same day. The transfer of Company X shares to Comany Y shareholders will be at a nominal value of $1.

company X will take over existing employee liabilities of US$ 500K of the company Y.

The fixed assets are fully depreciated (fair value assessed at US$ 100K) and Company X also received customer contracts annual revenue expected from these customer contracts is US$ 1.5mn in total and net profit margin varies from 5%-10%.

1. Is this considered a business combination or Asset purchase?

a. If it is a business combination:

i. How do I account for investment in standalone books. As subsidiary( there are no shares acquired in Company Y)? PPE? Intangibles?

ii. What values should I account it for

b. If it is an asset purchase

i. Should I recognize US$ 100K as PPE and the rest as intangibles

ii. What should be the useful life

2. What amount should I recognize for 45% of equity given up. Will it be a paid up capital amount of Company X thats US$ 2250 (45% X US$ 5000)

All companies are into operations and the core of the business is employees and equipments.

Appreciate your guidance.

Nice one. Thanks

Thank you very insightful!

Thanks Silvia, is this assessment applicable on acquisition of a company having a similar scenario as per your case study ?

Thanks for the article. I have a question. My client registered a company and used the newly registered company to acquire another company. The acquired company is an agent of a financial services company and earns income from its network of sub agents. Therefore it has no tangible assets. The net profit of the company was about CU500,000. The share capital of the acquired company is CU100,000 and it was acquired at CU5,000,000. The share capital of the acquiring company is also CU100,000. What are the accounting entries in this case.

Thank you Silvia for this Article. Very Helpful.

Hi Silvia,

Thank you for sharing your insight on the standard. It is very useful. Can you share the list of the US companies please, as I wish to understand these acquisitions in details.

Thanks a lot again for putting this down for us.

Hi Avantika, here’s the list with nice infographic. Best, S.

Hi Silvia, Thank you for sharing this insight. Very Helpful.

Hi Syliva,

If we involved into acquiring assets not a business and as a result no consolidation but assets and related liabilities being recognized in buyer’s separate SFP so, if the buyer paid a consideration which is higher than acquired net assets, Does the buyer recognize goodwill to his separate SFP ??

Well done! Simple and concise as always. Nice reading. 🙂

Thanks a lot, Sylvia.

I understand that IFRS 3 does a good job in differentiating the acquisition of an asset from a business. However, I will need to conduct a further study on how to identify the type of acquisitions done by firms in my locality. Something like an investigative assessment. I’ll use this as a guide.

Thanks once again.

If the company A received royal degree to own company B which owned by government.

There is input and output in B but accordingly, to the letter, Company B will dissolve and company A will stay and have a control.

So i think that it’s under common control and there is no purchase price to own B.

So this acqusition or not also if this acqusition i will transfer net assets in fair value or carrying amount.

There is no payment required from A to own B so is it process due to the Economic length market.

I think this out of IFRS3 Scope and the standards is silent in this case let me know please it very complex

Silvia dear,

As usual, you have presented a depth to understanding the changes to IFRS 3. The critical assessments and decisions to be made in deciding whether a business or asset is acquired must be done carefully to avoid accounting errors.

Methinks, a careful study and clear understanding of the Concentration Test is a critical success factor in making the right decision.

On the other hand, the harsh impact of these acquisitions on workforce and unemployment raises a lot of concern though it is also an opportunity for disengaged staff to up-skill and build capacity!

Thank you once more!