Can you capitalize demolition cost under IFRS?

Sometimes, when you need to acquire some land, you often purchase it with some obstacles on it – you know, old structures like buildings, roads, fences, and other things.

What to do with the costs incurred to remove these obstacles?

In today’s article, I respond to the question from Zareena, Malaysia:

“We are auditors and need your advice on the following situation for our client:

They have freehold land with building with total cost of CU 20 mil. acquired in 2015.

The building was partly demolished in 2017 just before the year-end and right after the year end, the demolition was completed and the client intends to sell the land.

The company never split the total cost of CU 20 mil. between the land element and building element and the depreciation of building was never charged.

What shall be done with the demolition cost and the old building?”

Answer: Determine the intention!

Hmmm, I came across the same question many times during my work and it seems many companies face more-less the same issue, just slightly twisted.

Let’s start with properties for own use under IAS 16 and let’s start with the demolition cost.

Demolition cost under IFRS

IAS 16 Property, Plant and Equipment does NOT directly address the demolition or removal of obstacles.

Under IAS 16 par. 16, the cost of an item of property, plant and equipment includes any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by the management.

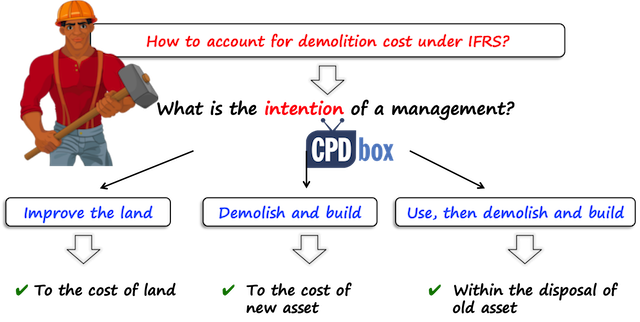

What was the intention of the management when they purchased the building together with the land?

Always look to the original intention or the reason why the building and land were acquired, because this will give you further direction.

There are few scenarios possible:

- Scenario n. 1: The company acquired land with building to demolish the building, make some improvements on the land and then sell the land.In this case, the intention was to acquire the land and the demolition cost of building is seen simply as a cost directly attributable to bringing the land to the condition to be operated in the manner intended by the management.Logically, you should add these demolition costs to the cost of the land as some land improvement.

- Scenario n. 2: The company acquired land with building to demolish the building, develop the site, build a new building and then use it.In this case, it’s a bit more complicated, because the intention is to have the new building and IAS 16 says in par. 58 that the building and land shall be classified as two separate items.Primary intention was to build a new building and therefore, demolition costs of old building are incremental to the new building, or in other words – you would not incur the demolition cost without wanting to build the new building.

So, in this case, you should capitalize the demolition costs to the cost of new building.

- Scenario n.3: The company acquired land with building, then used the old building for some short time and then demolished it with the intention to build a new building.In this case, the management’s intention at acquisition was to use the existing structure and thus demolition relates to the disposal of the old building.Therefore, you would not capitalize it to the cost of new building, but you would expense it as incurred.

You should also be careful about the fact that the demolition should occur within some reasonable time after the acquisition in order to prove the intention.

For example, you acquired the land and building in 2016 and you did nothing, and then in 2018 you decided to demolish the building and sell the land.

In this case, it’s questionable whether it was your intention to do so and whether you can simply say it’s the land improvement.

OK, that’s it for the demolition cost itself.

Carrying amount of old buildings

What should you do with the carrying amount of the old structures or buildings? Can you capitalize them to the cost of new buildings? Or expense?

There is no clear IFRS guidance on this point, but there are some accepted practices and other available guidance.

The main aspect to examine is how the old building was acquired and previously used:

- If you previously used the old building yourself and you decided to demolish it and build the new one, then you should simply derecognize the old building with gain or loss reported in profit or loss.More specifically, there’s usually some period between the decision to demolish and actual demolition, so you should probably accelerate depreciation over shorter remaining useful life and test the building for any impairment under

- If you acquired the land with old building to demolish it and build the new asset, the cost of the old building is incremental to the acquisition of the new assets and it’s appropriate to allocate the full purchase price to the land without splitting it.In most cases this would be acceptable, because you would rarely purchase highly valuable building with intention to demolish it, so rationally, the value of the old structure is low anyway.

Sometimes it’s not so simple.

It may happen that you acquired land with building with intention to demolish it, but that building has some fair value, it’s usable, but you want this location and you want to remove that structure anyway.

Here, there are strong arguments for not including the carrying amount of old building to the cost of the land, because IAS 16 requires splitting the land and building element and also, the building has its fair value regardless the buyer wants to demolish it or not.

In this case, you might need to allocate some part of the purchase price to the building and write it off in profit or loss. But again, you have to determine the fair value of old building really carefully with regard to the area, alternative use, etc.

Until now, I wrote about the case when you acquire building for your own use or for rentals – that would be more-less the same.

Developers: demolition within ordinary course of business

What about the developers and constructors who buy the lands with buildings and demolish them within the ordinary course of their business?

Here we are dealing with inventories under IAS 2 Inventories, so yes, the cost of old building and demolition cost are treated as inventories and it means that you need to keep inventories at lower of cost and net realizable value.

Example: Old building with land

ABC acquired a land with old building for CU 400 000 with intention to demolish the building and build the new one.

The building’s fair value is close to zero, because it is damaged and can be used only after significant investments into repairs and refurbishment.

ABC spent CU 20 000 to demolish the building.

In this case, it is appropriate to allocate all purchase price to the land.

As ABC plans to build the new building, the demolition cost is directly attributable to is and is included to the cost of the new building.

The entries are:

- Acquisition of the land:

- Debit PPE – Land: CU 400 000

- Credit Cash: CU 400 000

- Demolition cost:

- Debit PPE – New building: CU 20 000

- Credit Cash: CU 20 000

Here’s the video summing up this issue:

Do you have your own question? Send it here!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

15 Comments

Leave a Reply

Hi Silvia.

I got a situation where an existing asset is decommissioned and sold and some sales proceeds have been received. Some expenses also have been incurred to decommission the asset. Should we offset the expenses to decommission with the disposal proceeds to calculate disposal gain/loss?

Per IAS 16 – “The gain or loss arising from the derecognition of an item of property, plant and equipment shall be determined as the difference between the net disposal proceeds, if any, and the carrying amount of the item.” How does net proceeds differ from gross proceeds?

Thanks

If you have land for a number of years and that land has a building, but you don’t use the building, it is owed by someone else. You are finally able to purchase the building and you demolish it as you want to use the land for something else (not a new build). Is the demolition added to the cost of the land?

Hi Silvia

My question is if a company acquires a building without the land for which it pays a head lease and demolish the building, then how you would account for the costs of the intention of the management is

to build a new building only.

Hi Silvia, i hope you are well.

We have a scenario for a demolished building. The municipality had demolished our head quarter office in year 2020 even with out considering a compensation during that time. Recently, the municipality has been forced to pay the building value estimated in current market price, though the money not released until now. We are currently implementing ERP in the company and we should migrate our data to oracle fixed asset module. So what entry should i made assuming the following data. Cost 400m,accumilated depreciation 250m. The estimated value to pay by the municipality 500m.

Hi,

Is there any IFRS accounting standard that will explain the proper method to account for demolition cost after impairment of a building?

As in should it the demolition costs be capitalized of expensed?

Hi Silvia,

We, the client rented a land from a landlord and we constructed a building in the land. Just before the capitalization of the building (Work was not completed 100%) we got notice from the authority to vacate the land as the country had planed to develop that area to another level. So all the people from that place had to vacate the land.

Now in this situation we had to demolish the building and we stopped that division for ever. My question is what would be done for the construction cost and the demolition cost in our books?

Hi Sajeev, I am afraid you have nothing to capitalize the demolition cost to – because you will never have the asset.

Hi Silvia,

Thanks for such a helpful article. Actually i have a question. our company have a concession contract with our parent company, and fixed asset are belongs to our parent company, in our books as Right to use of Assets under IFRS-16. At the time of concession contact our company has an intention for expansion in business in future. So now at the time of expansion they relocate old pants (belongs to parent company) to other place. so in this case Our Company can capitalize these relocation cost as there are “directly attributable cost with expansion decision” or under “site preparation point as in IAS-16” or straight forwardly expensed out?

Many Thanks,

In other case, if the land is freehold and in the country’s law all lands are owned by the government, how can we account the free hold land based on IFRS requirement? In local GAAP it is not allowed to record lands.

Good explanation. What if the land and building are under Investment property and part of the building demolished completely to construct a new one. In this case do we need to charge disposal loss (fair value of the demolished building) to income statement and capitalized the demolishing cost to the new building??

Dear Silvia ,

We are in construction industry our project is approximately finished .We shifting material from site to our warehouse we need container to place this material .Can we recognize these container as fixed asset ,company have no more project these container with material hand over to our other company in group .

Regards ,

Rana Atif

Hi Silvia, if a demolition is required to remove a stairwell in order to install an elevator, will the cost of demolition be capital or expense? Thank you

Hi Mel,

the same principle as described in this article applies 🙂 S.

If we can capitalize demolition cost, and in return, we sold demolition waste, should the construction waste be deducted from the demolition costs?

Hi Hossam,

under article 21 of IAS 16, this is incidental income and is recognized in profit or loss although yes, it would be logical the other way.