How to deal with different useful lives of PPE within the group?

Here I respond the question asked by Junic from Singapore:

We have a head office in Singapore and subsidiaries in various countries.

The headquarters of the parent company set the useful lives of the property, plant and equipment (PPE) for the whole group and subsidiaries have to depreciate their PPE over these useful lives set by the parent.

But individual countries have their own laws or rules on the useful lives that are not the same as what the parent company prescribes. Also, auditors of the subsidiary insist on using useful lives in line with the parent’s policy.

How can this be handled in the financial statements?

Answer: Several solutions are possible

This is a great question because it happens on a regular basis and many companies within the same group use different useful lives of their assets. And, auditors insist on depreciating these assets over the uniform useful lives throughout the group.

I personally don’t like it. Yes, it is very practical – no dispute on it.

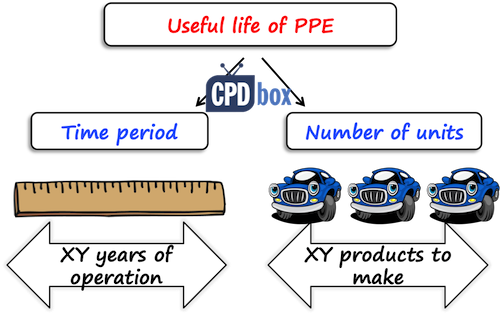

But, the standard IAS 16 says that the useful life of an asset is determined based on expected utility of that asset to an entity.

According to IAS 16 par. 6, the useful life is either:

- The period over which an asset is expected to be available for use by an entity, or

- The number of production or similar units expected to be obtained by that entity.

So, the useful life is specific to the individual asset and individual entity.

It is quite possible that the parent can use the same type of asset for a longer period than its subsidiary and as a result, both can apply different useful lives.

Just imagine one subsidiary operating in northern Canada and one operating in India. Totally different climates – one is cold, one is warm.

They bought the same drilling machine that will operate outside. It is quite probable that the subsidiary in Canada will use the same machine for the shorter time that the company in India just because the temperatures are much lower, the ground is harder and the drilling machine would be consumed earlier than the one in Indian warm weather.

So it’s normal in this case to have different useful lives for the same assets.

Now I can hear you saying – but, when you consolidate, IFRS 10 says that the companies within the group MUST apply the same accounting policies!

Yes, that’s true, but the useful life is NOT an accounting policy, but an accounting estimate and it is specific for each company and each asset I would say. So it’s permitted to apply different accounting estimates based on the specifics of that company.

However, in practice, it is very common that the parent prescribes the useful lives of all assets within the group and although it might not fully reflect the reality, it is widely accepted.

So what to do when the local useful lives or depreciation rates are different for tax purposes than the group rate?

There are several solutions possible:

- Subsidiary depreciates its PPE over the same useful lives as its parent in its own local accounting records. Here, if the tax depreciation rules are different, subsidiary must recognize deferred tax.

- In its local accounting books, the subsidiary depreciates its PPE over the useful life as prescribed by the local legislation. When the subsidiary prepares the reporting package for the consolidation purposes, it will make the adjustment to align useful lives with the group’s policy and again, the deferred tax would be required in that consolidation package.

- The parent can make the adjustment when consolidating all subsidiaries, but if the parent owns number of subsidiaries, it would be extremely demanding to keep track on adjustments of every single subsidiary.

The easiest approach is probably the first one, when the subsidiary just applies the group’s rates in its own local accounting books and makes the adjustment for the deferred taxation.

Yes, it is true that in this case, PPE might not reflect the subsidiary’s reality, but if the subsidiary does not need to submit the financial statements to some public market like stock exchange and reports just to tax office and to the parent, it would be acceptable.

If the subsidiary is big enough and it’s shares or other instruments are traded publicly on the stock exchange or needs to share its individual financial statements with the wide range of users, then I would go for the second option and make adjustment in the consolidation package.

Example: Handling different useful lives within the group

Subsidiary acquired a building with cost of CU 120 000. Local tax legislation prescribes to depreciate buildings straight-line over 40 years, but the group’s policy is to use the buildings for 30 years and then sell them. Tax rate in subsidiary’s country is 20%.

The first approach: The same useful lives

Subsidiary depreciates the building over 30 years exactly as its parent.

The annual depreciation is then CU 120 000/30 = CU 4 000. The carrying amount at the end of year 1 = CU 116 000 (120 000 – 4 000).

For tax purposes, it is possible to deduct CU 120 000/40 = CU 3 000. The tax base at the end of year 1 = CU 117 000 (120 000 – 3 000).

As the tax base is different than the carrying amount, the deferred tax must be recognized: 20%*(117 000-116 000) = 200 (deferred tax asset).

Journal entries – in subsidiary’s individual financial statements:

- Depreciation: Debit P/L Depreciation: CU 4 000 / Credit PPE – Accumulated depreciation: CU 4 000

- Deferred tax: Debit Deferred tax asset: CU 200 / Credit P/L – Deferred income tax: CU 200

There is NO need to make any consolidation adjustment.

The second approach: Adjustment in the reporting package

Subsidiary depreciates the building in line with the local legislation.

The annual depreciation is then CU 120 000/40 = CU 3 000. The carrying amount at the end of year 1 = CU 117 000 (120 000 – 4 000).

Tax depreciation is the same, therefore no deferred tax arises in the local books.

Journal entry – in the subsidiary’s individual financial statements:

- Depreciation: Debit P/L Depreciation: CU 3 000

- Credit PPE – Accumulated depreciation: CU 3 000

When making consolidation, consolidating adjustment will be made in the group’s financial statements:

- Aligning the depreciation:

- Debit P/L Depreciation: CU 1 000

- Credit PPE – Accumulated depreciation: CU 1 000 (difference between the group’s policy and local tax rules)

- Deferred tax on adjustment:

- Debit Deferred tax asset: CU 200

- Credit P/L – Deferred income tax: CU 200 (CU 1 000*20%)

From the above examples it’s clear that from the group’s view, it’s easier to use the same accounting estimates (approach 1) to reduce the amount of adjustments and journal entries.

I put this answer into a video and you can watch it here on YouTube:

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

19 Comments

Leave a Reply

I have a question, is it okay to follow different type of depreciation calculation method for Parent company and its Subsidiary. Like X company holds 51% of shares in Y company. X company following Straight line method and Y company following Written down value. Is it okay to continue with this ?

Thank you, Silvia, I did not realize that depreciation rates are in fact accounting estimate and not accounting policy and there can be different rates within the group. But what about materiality? Our branch is relatively small…

Hi Andy, yes, it can happen that the whole subsidiary is relatively small or immaterial for the group. In my good old auditing times, we used to call it “rounding difference”. So, if your company is a rounding difference to the group, then I guess no one will care if you don’t apply the group rates, is it? It is really not likely to be material. S.

Hi Silvia,

Under IFRS is it possible for an entity to use different useful life of cars within the same asset (e.g for old cars 20%, and for new cars 10%)?

HI Silvia, Please brief the difference of Useful Life and economic life of asset.

Economic life = period over which an asset is capable of bringing the benefits; useful life = period over which YOU plan to use the asset. I.e. a car can have an economic life of 6 years, but your policy is to sell cars after 4 years and then get the new ones – so the useful life is 4 years only.

Hi Silvia, could you advice if company plan to change usefull life of PPE with goal to be in line with Group policy. should we recalculate it for every assets retrospectively or could just apply prospectively?

Prospectively as it is a change in the accounting estimate.

Where can you find the standard useful lives under IFRS?

Hi Silvia!, excellent answer about different useful lives according to IAS 16.

I have a question about documenting this “useful lives estimates”, how technical this estimate can be?.

Not only to satisfied external auditors, mostly to reflect the consumption pattern of the asset. I’ve read in this webpage (https://inspire.partica.online/inspire/inspire-apr-2017/roundtable/aligning-asset-and-financial-management) about the different points of view between engineers, auditors and economists about this.

I work in the banking industry and because financial instruments can be more material than PP&E, sometimes banks don’t look at this estimates with the same importance as “PD or LGD” on IFRS 9.

I do think is important to estimate useful lives with a technical approach (ISO 55000 – Asset Management for example) because this can have a meaningful impact in the financial statements, efficiency ratios and profitability business units analysis for banks, if you estimate correctly an asset’s useful life, there are a lot of benefits: A risk/estrategy approach about acquisitions, maintenence and replacement

Greeting Silvia,

Just wanted to know for example the Company has two buildings and similar assets attached to it are depreciated at a different rates based on their assessment of the estimated useful lives of the assets. Example in one building the elevator was estimated to have useful life of 5 years and another building the elevator is estimated to have useful life of 10. One building estimated to have useful life 0f 20 year and another building is estimated to have useful life of 40 years. To show better profitability also they can change the estimated useful lives. What does the IFRS say about this.

I came to know that it is possible to charge depreciation based on unit of production method. My doubt here is a Company is having a capacity to generate output of 100 units in an year. But during the year 1 it produces 25 units only and it expects to produce 35 units on second year and 45 units on third year and so on. The Company charges depreciation based on the above said progressive method. Is this a correct method.?

Yes, as soon as it reflects your estimate about the asset’s usage.

Dear Silvia,

I am a masters student in management; majoring in financial analysis and audit studying in BELGIUM. but I have a very big issue with numbers because I am not good at numbers at all. thus far, after getting to know what you do here, i truly believe you could my road-map to get to know how to play with accounting. so I hope you will be able to see my email so we can exchange some ideas and see how I can start my course with you. looking forwards to

Dear Madam,

I have a question regarding IAS 16 PPE

I am working in telecoms industry, and deal with turnkey projects for involving setting up of Transmission equipment and towers etc. I would like to know how in the asset register should we record such projects ? Should i break them on unit by unit basis or group basis ?

1) Example :A Microwave link requires 3 items to work an Antenna, IDU (Indoor unit) and ODU (Outdoor unit) , should i treat them as separate items in the asset register or treat it as one link (unit) ? Please note they all have same economic life and commissioning can only take place when all the 3 parts are in place.

2) The other questions is we have left over spares for projects which are fully commissioned and are being depreciated in our books. How do we deal with such remaining spares ? It is difficult to attach value to such spares as they come together with the assets, and not ordered separately as stock.

Regards,

Sidharth

Hi Silvia,

Trust that you are doing good.

I am a having a small issue on useful life time of the asset. Lets say there is an asset which is having a useful life time of 5 years (according to accounting policies). But when it comes to the financial statements, assets have been fully depreciated before the expected useful life of 5 years. Lets say on 4th year it has been fully depreciated. Is a scenario like this permitted by IAS 16?

Hi Silvia,

In 1st approach, as per local tax rules depreciation per year is less than computing as per parent thus it will result in lesser profits as per accounting records as compared to tax books. May I know why it will not create deferred tax liability and thus entry should be Dr. Deferred tax expense Cr. Deferred tax liability?

If you have higher tax profits than accounting profits, it means that NOW you pay higher tax than you should have paid as per accounting. E.g. accounting profit is 1 000, tax profit is 1 500, tax rate is 20% – you pay tax of 300 (on 1 500), but under accounting books, you would pay just 200. This difference of 100 is deferred tax asset – it’s something that “tax office owes you to the future”, in other words, you will reverse it and pay less tax in the future. Hope this explanation helps!

thanks.