IFRS 16 Leases Explained: Full Guide + Free Video & Checklist

Updated: May 2025

IFRS 16 changed lease accounting forever. Lessees now bring almost all leases onto the balance sheet — no more hiding operating lease liabilities in the footnotes.

In this guide, you’ll learn how IFRS 16 works in practice, including main rules, two free video lectures and practical checklist to download and use as your reference.

Jump to section:

1. Free VIDEO lecture: Overview of IFRS 16 Leases

2. Objective of IFRS 16

3. What is a lease under IFRS 16?

4. Accounting for leases by lessees

5. Free VIDEO lecture: Example of lease accounting step by step

6. Accounting for leases by lessors

- 6.1 Classification of leases

- 6.2 Finance lease: Initial measurement

- 6.3 Finance lease: Subsequent measurement

- 6.4 Operating lease

7. Sale & leaseback transactions

8. Presentation and disclosures in line with IFRS 16

9. DOWNLOAD IFRS 16 Practical Checklist

10. Further reading&learning

1. Overview of IFRS 16 Leases (free VIDEO lecture)

2. Objective of IFRS 16

The objective of the standard IFRS 16 Leases is to specify the rules for recognition, measurement, presentation and disclosure of leases.

But, why is there a new lease standard when we had an older IAS 17 Leases?

The main reason is that under IAS 17, lessees were still able to hide certain liabilities resulting from leases and simply not present them on the face of the financial statements.

I’m talking about operating leases, especially those with non-cancellable terms.

Under the new standard, lessees will need to show all the leases right in their statement of financial position instead of hiding them in the notes to the financial statements.

Note: IFRS 16 applies for the periods starting on or after 1 January 2019 (careful about the comparatives).

Return to top

3. What is a lease under IFRS 16?

A contract is or contains a lease if it conveys the right to control the use of an identified asset for a period of time in exchange for consideration (IFRS16, par.9).

This definition of lease is much broader than under the old IAS 17 and you must assess all your contracts for potential lease elements.

You should carefully look at:

- Can the asset be identified? E.g. is it physically distinct?

- Can the customer decide about the asset’s use?

- Can the customer get the economic benefit from the use of that asset?

- Can the supplier substitute the asset during the period of use?

If the answer to these questions is YES, then it’s probable that your contract contains a lease.

As I wrote in my article about comparison of IFRS 16 and IAS 17, the impact of this new broader definition can be quite big, because some service contracts (with payments recognized directly in profit or loss) can now be considered as lease contracts (with necessity to recognize right-of-use asset and lease liability).

Under IFRS 16, you need to separate lease and non-lease components in the contract.

For example, if you rent a warehouse and rental payments include the fees for cleaning services, then you should separate these payments between the lease payments and service payments and account for these elements separately.

However, lessee can optionally choose not to separate these elements, but account for the whole contract as a lease (this applies for the whole class of assets).

Return to top

4. Accounting for leases by lessees

Warning: Lessees do NOT classify the leases as finance or operating anymore!

No classification!

Instead, lessees account for all the leases in the same way.

4.1 Initial measurement

At lease commencement, a lessee accounts for two elements:

- Right-of-use asset Initially, a right-of-use asset is measured in the amount of the lease liability and initial direct costs.Then it is adjusted by the lease payments made before or on commencement date, lease incentives received, and any estimate of dismantling and restoration costs (remember IAS 37).

- Lease liability The lease liability is in fact all payments not paid at the commencement date discounted to present value using the interest rate implicit in the lease (or incremental borrowing rate if the previous one cannot be set).These payments may include fixed payments, variable payments, payments under residual value guarantees, purchase price if purchase option will be exercised, etc.

Let me outline the journal entries for you:

- Lessee takes an asset under the lease:

-

Debit Right-of-use asset

-

Credit Lease liability (in the amount of the lease liability)

-

- Lessee pays the legal fees for negotiating the contract:

-

Debit Right-of-use asset

-

Credit Suppliers (Bank account, Cash, whatever is applicable)

-

- The estimated cost of removal, discounted to present value (lessee will need to remove an asset and restore the site after the end of the lease term):

-

Debit Right-of-use asset

-

Credit Provision for asset removal (under IAS 37)

-

4.2 Subsequent measurement

After commencement date, lessee needs to take care about both elements recognized initially:

- Right-of-use asset

Normally, a lessee needs to measure the right-of-use asset using a cost model under IAS 16 Property, Plant and Equipment.It basically means to depreciate the asset over the lease term:-

Debit Profit or loss – Depreciation charge

-

Credit Accumulated depreciation of right-of-use asset

However, the lessee can apply also IAS 40 Investment Property (if the right-of –use asset is an investment property and fair value model is applied), or using revaluation model under IAS 16 (if right-of-use asset relates to the class of PPE accounted for by revaluation model).

-

- Lease liability

A lessee needs to recognize an interest on the lease liability:-

Debit Profit or loss – Interest expense

-

Credit Lease liability

Also, the lease payments are recognized as a reduction of the lease liability:

-

Debit Lease liability

-

Credit Bank account (cash)

If there is a change in the lease term, lease payments, discount rate or anything else, then the lease liability must be re-measured to reflect all the changes.

-

4.3 Is this too complicated? Exemptions exist!

If you got this far in reading this article, maybe you find it overcomplicated, especially for “small” operating leases.

Here’s the good news:

You do NOT need to account for all leases like described above.

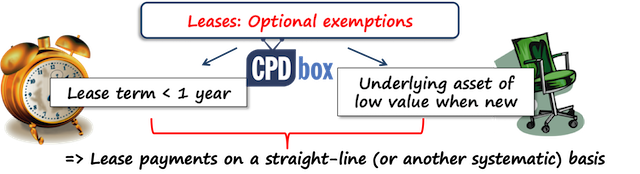

IFRS 16 permits two exemptions (IFRS 16, par. 5 and following):

- Leases with the lease term of 12 months or less with no purchase option (applied to the whole class of assets)

- Leases where underlying asset has a low value when new (applied on one-by-one basis)

So, if you enter into the contract for the lease of PC, or you rent a car for 4 months, then you don’t need to bother with accounting for the right-of-use asset and the lease liability.

You can simply account for all payments made directly in profit or loss on a straight-line (or other systematic) basis.

Return to top

5. Example: Lease Accounting by the Lessee (free video lecture)

6. Accounting for leases by lessors

Nothing much changed in accounting for leases by lessors, so I guess you already are familiar with what follows.

6.1 Classification of leases

Unlike lessees, lessors need to classify the lease first, before they start accounting.

There are 2 types of leases defined in IFRS 16:

- A finance lease is a lease that transfers substantially all the risks and rewards incidental to ownership of an underlying asset.

- An operating lease is a lease other than a finance lease.

IFRS 16 (IFRS 16, par. 63) outlines examples of situations that would normally lead to a lease being classified as a finance lease (and they are almost carbon copy from older IAS 17):

- The lease transfers ownership of the asset to the lessee by the end of the lease term.

- The lessee has the option to purchase the asset at a price that is expected to be sufficiently lower than the fair value at the date of the option exercisability. It is reasonably certain, at the inception of the lease, that the option will be exercised.

- The lease term is for the major part of the economic life of the asset even if the title is not transferred.

- At the inception of the lease the present value of the lease payments amounts to at least substantially all of the fair value of the leased asset.

- The leased assets are of such a specialized nature that only the lessee can use them without major modifications.

6.2 Finance lease: Initial measurement

At the commencement of the lease term, lessor should recognize lease receivable in his statement of financial position. The amount of the receivable should be equal to the net investment in the lease.

Net investment in the lease equals to the payments not paid at the commencement date discounted to present value (exactly the same as described in lessee’s accounting) plus the initial direct costs.

The journal entry is as follows:

-

Debit Lease receivable

-

Credit PPE (underlying asset)

6.3 Finance lease: Subsequent measurement

The lessor should recognize:

- A finance income on the lease receivable:

-

Debit Lease receivable

-

Credit Profit or loss – Finance income

-

- A reduction of the lease receivable by the cash received:

-

Debit Bank account (Cash)

-

Credit Lease receivable

-

Finance income shall be recognized based on a pattern reflecting constant periodic rate of return on the lessor’s net investment in the lease.

IFRS 16 then also specifies accounting for manufacturer or dealer lessors.

Return to top

6.4 Operating lease

Lessor keeps recognizing the leased asset in his statement of financial position.

Lease income from operating leases shall be recognized as an income on a straight-line basis over the lease term, unless another systematic basis is more appropriate.

Here you can see that the accounting for operating leases is asymmetrical: both lessees and lessors recognize an asset in their financial statements (it’s a bit controversial and there were huge debates around).

7. Sale and Leaseback transactions

A sale and leaseback transaction involves the sale of an asset and the leasing the same asset back.

In this situation, a seller becomes a lessee and a buyer becomes a lessor. This is illustrated in the following scheme:

Accounting treatment of sale and leaseback transactions depends on the whether the transfer of an asset is a sale under IFRS 15 Revenue from contracts with customers.

- If a transfer is a sale:

- The seller (lessee) accounts for the right-of-use asset at the proportion of the previous carrying amount related to the right-of-use retained. Gain or loss is recognized only to the extend related to the rights transferred. (IFRS 16, par.100)

- The buyer (lessor) accounts for a purchase of an asset under applicable standards and for the lease under IFRS 16.

- If a transfer is NOT a sale:

- The seller (lessee) keeps recognizing transferred asset and accounts for the cash received as for a financial liability under IFRS 9 Financial Instruments.

- The buyer recognizes a financial asset under IFRS 9 amounting to the cash paid.

8. Presentation and disclosures in line with IFRS 16

Lessees must:

- Present right-of-use assets either separately or within the same line item as similar assets.

- Show lease liabilities separately or as part of other financial liabilities.

- Disclose:

- Maturity analysis of lease liabilities

- Expense from short-term and low-value leases

- Cash outflows for leases

- Additions and carrying amounts of right-of-use assets

- Significant judgments (e.g., lease term, discount rate)

Lessors must disclose:

- Risk exposure from residual value guarantees

- Selling profit or loss for manufacturer/dealer lessors

- Income from variable lease payments

9. DOWNLOAD IFRS 15 Practical Checklist

10. Further reading and learning

Explore more on IFRS 16: Visit this page to access the full library of all IFRS 16-related articles, videos, and examples published by CPDbox.

Learn IFRS with real examples – not just theory.

Any questions? Please let me know below, thank you!

Return to top

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

202 Comments

Leave a Reply

Dear Silvia,

Great as usual, thanks.

I have one question. Assume Company XYZ rent a building for it’s office. The contract agreement is for 6 months. XYZ have been using this building for the past 3 years and was renewing the contract every 6 month. Is this lease exempted from IFRS 16 for < 12 months criteria? I'm thinking "Substance over form".

If it is exempted, don't you think IFRS 16 is prone to manipulation of "off balance sheet financing"?

Thanks

Hi Silvia,

I hope this massage find you well

I have enquiries regarding the IFRS 16, Our company signed land lease agreement with government for (50) years extendable but without buying option the annual rent is $(1.3 million).

The questions are:

1- Does the IFRS 16 apply on land lease? if Yes

2- Considering there are no land depreciation as per IFRS, how we will account for it under the IFRS16?

Your feedback will be highly appreciated

Regards,

Really helpful, thanks. One question:

Initial recognition journal 3 is Debit Right-of-use asset, Credit Provision for asset removal for the discounted value of cost of removal. Say that estimated cost is £100k and the discounted value at start is £70k – what are the entries to increase that provision up to £100k by the time it needs to be settled? Where does the additional £30k get debited, and when?

Hi silvia,

i have a query regarding sale and lease back transactions. i have provided here an example please help me out:

Sale value at the date of sale: USD 25m

FV at the date of sale USD 23m

Gain on sale: USD 5 m

sale qualifies ifrs 15

present value of new lease liability USD 15m.

what would be the accounting treatment for this?

Hi Silvia,

Thanks for your wonderful articles. I always find them extremely helpful for understanding the concept.

Here, I have one question related to Accounting for finance lease by lessors. As per the articles lease receivable should be equal to the net investment in the lease that is equals to the payments not paid at the commencement date discounted to the present value plus direct costs. Shouldn’t we take the fair value of leased assets at the commencement date plus direct costs?

Hello, Pramod, thank you! The answer is no. S.

Hi Silvia, previously, a Company, which used to obtain vehicles on say vehicle lease finance for a period of 5 years and the asset used to be jointly registered until the lease was padi. In such cases the asset was debited in the books of lessee and the vehicle lease finance was shown as lease liability. Under IFRSs 16, will the vehicle in PPE schedule be replaced by RIght of use asset?? Or is it ok to show as vehicles as was shown by lessee when IAS 17 was in place

IFRS 16 C.17 mention:

If a lessee elects to apply this Standard in accordance with paragraph C5 (b), for leases that were classified as finance leases applying IAS 17, the carrying amount of the right-of-use asset and the lease liability at the date of initial application shall be the carrying amount of the lease asset and lease liability immediately before that date measured applying IAS 17. For those leases, a lessee shall account for the right-of-use asset and the lease liability applying this Standard from the date of initial application.

Hi, Silvia, What will be the treatment of previously recognized finance lease when my year end is at 31 march 2019? should i account for from 2019 or should i wait to end the year 2019?

Well, I don’t quite understand the issue here. When your year-end is 31 March 2019, then you are making a transition to IFRS 16 from 1 April 2019… S.

Hi Silvia, thanks for this. I may be misunderstanding but does this mean instead of recognising a rental expense (for a lease on a building) the P&L charge is only shown through depreciation and interest therefore improving our EBITDA position?

Yes, something like that 🙂

Hi Silvia

I need some additional clarification in terms of the below point from IFRS 16, B35

IFRS 16, B35: “If only a lessor has the right to terminate a lease, the non-cancellable period of the lease includes the period covered by the option to terminate the lease.

Question: Practicable description of “the covered period” is not clear. Could you, please, bring an example in terms of Telecommunication, rent for rent of land of stations.

Hi Silvia

What if the lease agreement, other than rent, also included the fixed charge of monthly building management fee with effect from the commencement of the lease but subject to adjustment during the lease period.

Thanks!

Hi, What happens when lease incentive is higher than the ROU asset and ROU asset is negative?

There could be many scenarios such as either party terminated early or a mutual agreement to provide higher lease incentive.

Using common sense, this should not be allowed otherwise companies can actually make profits when leasing but i came across situation when it is the case. Appreciate your thoughts and thank you in advance.

Thank you so much for your quick reply, Silvia.

Hi Silvia! I have two questions.

1. Does this mean that we will create a new account, i.e., Right-of-use account (ROU), in our chart of accounts? Or the ROU was used for discussion purposes only.

2. We are renting an office space in a condominium hotel. Lease term is 5 years subject to annual escalation clause. Is this covered by IFRS 16?

Thank you.

Dante

Hi Dante,

1. Yes, you may.

2. Yes, it is. S.

I want to get a detailed notes of IFRS and IAS. How can i contact you for this

Hi Sylvia ! thank you for your insightful articles, really finding it easy to follow and understand.

I have a question on IFRS 16 please – what happens on consolidation? what would be the accounting entry to reverse the right of use of the asset, liability and the income statement charge ( interest + depreciation) please? Do you have any examples you could share with us please?

Hi Daniela, are you asking on consolidation when the lease is intragroup? Well, you need to reverse all entries as if they had never happened, since the inception of the lease. Everything booked to profit/loss in previous years is reversed via equity (retained earnings). S.

Hi Sylvia,

We have some leases for offices for which the initial duration of the contract has ended and since then, the contract is silently renewed every year. In this cases how would you determine the lease period which will be used for the calculation of the RoU and Lease liability?

Many thanks and regards,

Stefanos

Hi Stefanos, I think this can help. S.

I have a question on subcontractors e.g XYZ has over 3,000 small captive (regular) subcontractors providing their owned vehicles to the company for freight services under the following terms:

• XYZ controls and direct the use of the vehicle to customer location.

• The small contractor has only one to two trucks and works predominantly for XYZ.

• A yearly renewable contract, but majority serviced XYZ for over 3 years and some does not have a signed contract.

• Compulsory attendance at health and safety training held by XYZ sales and delivery procedures training.

• Wear XYZ uniforms and interact with the customers and customer sign acceptance of delivery on XYZ equipment

• On XYZ payment system ( e.g records number of deliveries to calculate monthly subcontractor payment)

• Subcontractor takes the vehicle home daily after working hours

• Any refund for loss of customer parcels are paid by XYZ and amount deducted from subcontractor payments, if the latter is found at fault.

Appreciate your view on whether we should account for 3,000 under Portfolio lease with following:

• Lease term 3 years

• Discount rate is the XYZ’s incremental borrowing rate

• Lease payment is estimated by reference to market vehicle rental rate ( monthly rate)

Or whether we keep those as sub-contractors expense.

Many thanks

Rama

How does the accounting entry goes for sale and lease back on the sellers side innboth the condition?

Hi Silvia,

Thanks for your article.

With respect to applying the short term 12 month exemption:

If we have a building lease terminating on 30.06.2019 however exit terms (for ex an exit fee etc) have all been agreed formally and in writing by 31.12.2018, then would we still be able to apply the short term exemption and continue accounting for the lease as a normal operating lease until termination?

Thanks

Steven

Hello,Silvia! Thanks for this article! Have a question about exemption:

1. Leases with the lease term of 12 months or less with no purchase option – What about lease contracts with the lease term of less than 12 months BUT with the right for prolongation or if contract has wording as following,for example: “the term is min 8 months/ max 13 months” or min till February 11,2019 (and this is the term of 10 months) and max till May 11,2019 “. How these leases should be recognised by lessee?

Hi Olga, as for the lease term, please look here. It solves very similar cases and I have nothing to add 🙂

Hi.. Assuming that the underlying asset is an investment property (land) in the lessee’s books, what happens to the right of use asset at the end of the lease term in the lessee’s books under an operating lease?

The right of use asset has been measured at FV at the end of each year and the relevant FV adjustments have also been made,

Please recommend the relevant accounting entry as well.

Hi Silvia, if we purchased a software, naturally we can apply IAS 38. But if there are any licensing fees to use that software, can we treat the licensing fee under IFRS 16?

Hi Sylvia,

First of all, thank you for your amazing contribution to the understanding of IFRS. The article is great, but I would like to point out that when the answer is “yes” to the following question, then you probably DO not have a lease contract:

“Can the supplier substitute the asset during the period of use?

If the answer to these questions is YES, then it’s probable that your contract contains a lease.”

Thank you for the insight. Keep the good work.

Hi Sylwia,

Thank for your articles.

Can you please share your approach in term of Abstract:

I have more details in the Abstract:

Current Monthly Rent include:

Base Rent

Operating Expenses

Parking

VAT Base Rent

VAT Operating Expenses

VAT Parking

What is the Right-of-use asset ?

How it should be settled?

thank you in advance,

Krystyna

Krystyna, if you can claim VAT back, then don’t include it to ROU. If you opt not to separate as a lessee, then you can include everything else.

And also please clearify how to seperate Lease from service contract?

Hi, Thanks for the valuable information. I need to ask about the journal entries in the book of Lessee . Suppose i have take a building on rent for the period of 10 years. I am lessee and building is identified asset and i have right to use. i am paying 100000 per month. Now what is journal entry for this payment. Whether i have to show the building in my books as right to use asset and Lease liability and depreciate the amount of lease liability over the Lease period. Please clearify the journal entries in the book of Lessee

Hi Meen, I think you should check out this article – it comes with example.

Hi Silvia, thank you for your article.

Will you please answer the question about lessor accounting – finance lease.

IFRS 16, 70: “…the lease payments included in the measurement of the net investment in the lease comprise the payments …that are not received at the commencement date”. What if lessee pays some amount before the commencement date (after the inception date)?

I think it should be accounted for as follows:

a) Debit Lease receivable Credit PPE

b) Debit Cash Credit Deferred income

and it will be recognised in income evenly throuthout the lease term.

Am I right?

Dear Silvia :

Are the amounts paid at the beginning of the lease as costs added to the rent payments, such as:

Amounts paid for the first time against the rental of a building

Commissions

Thank you

Hi Silvia, I have Question Please ( If I have rent contract for 5 Years Contains Base rent of 10,000,000 Per Year and 200,000 As service Charges Yearly 5% annual increment As per IAS 17 Total Base rent of the five years Amortized equally on monthly basis. shall we do the same for Service charges ?

Thanks madam Sylvia. Is IFRS effective starting on 1 January 2018 or 1 January 2019. Thanks

It’s written above in the article – 2019.

Hi does IFRS 16 apply to land taken on lease ?

If yes how do we depreciate the right of use asset since land is generally not depreciated.

Hi Dhaval, you are not depreciating the land, you are depreciating only the right to use the land over the lease term.

In this case the lease term is your asset’s useful life.

Hi Mohamed

if ROU (financing agreement and the option selling price $ one )and time is 10 years

what is cost of land after 10years

Thank u so much for your explanation on z new IFRS 16

dear ma’am, i have a question, in case of low value or less than 12 months, is exemptions applies only in operating lease, and for lessee. does it applies for lessor or for finance lease???

thanks

thank you dear ma’am

Thank you Silvia, I appreciate

Hello Silvia M,I request you to upload a page consisting of Manufacturer dealer lessor Journal entries format and treatment of IDC (Initial Direct Cost).

What about subleasing? How do we account for it?

If the sublessor will recognize in its books the right-to-use asset as a lessee, will it also recognize in its books a lease receivable as a lessor?

For the sublessee, will it recognize in its books the right-to-use asset as a lessee?

Hi, if the sublease is finance, then the intermediate lessor debits the net investment in the lease and credits right-of-use asset, the difference is recognized in profit or loss.

Hi Silvia,

How about if you are an intermediate lessor in a building where you lease office space and you sublet a portion of the space.

In this case, it is determined that the sub-lease is an operating lease.

Are you able to net the sublease income earned against the related lease expense (the depreciation)?

Furthermore – can you argue that the depreciation of the Right of Use Asset can be classified under G&A (and not with other depreciation?).

Under the current standards, I believe you are able to net the sublease income against the leasing expense.

Thank you in advance.

Ray

Following. I have the same question regarding subleasing the office.

Hi Sylvia,

Good afternoon! (PH time)

I have a question. Is IFRS 16 applicable to contract of easement of right of way?

Thank you and God bless,

Rose

Hi Silvia

Company A invests in power plant to produce and supply electricity under a PPA (Power Purchase Agreement) to the national grid (govt owned organisation). Assume PPA agreement is for 10 years with possibility of extending for another 10 years. would you consider this as a lease scenario?

Thanks

Hans

Hans, under older IAS 17 yes, that would be a lease because the criterion was that the customer has the right to substantially all of the asset’s output.

Under new IFRS 16 you need to assess whether the customer has the right to direct how the identified asset (power plant) will be used. You must analyse the decision-making rights over the power plant – e.g. dispatch rights (who determines the optimal output of the plant?), curtailment rights, etc. – who has these rights? If it’s a customer (national grid), then well, you have a lease there. It’s not so straightforward and you need to analyze the contract carefully. S.

thanks Silvia. Customer has no decision making rights on the P Plant. However, in the event when output is below the PPA Kwh, Company has to compensate customer on the shortfall.

Thank you soo much .

this was really helpfull .

but i really dont understand why we should use straight line method in recognize revnues or expenses in case of operatin lease i think this will ignore the inflation impact and will show no gross in the company profit if the payments varies from year to another , and in same time iam as alessor cannot ask the lesee to pay more than what was agreed in the contract as payment term .

thanks

Kindly upload some illustratives on sale and lease back transaction when the transaction is a sale as per IFRS 15. Thanks!

Thank you for the insight. Keep the good work. GBU

Thanks

I have questions related to (IAS 17) old standard.

Our company is doing the convergence to IFRS, as required by regulator from 1-1-2017.We didn’t apply IFRS 15 and therefore for lease we will adopt the old standard. We signed agreement with government (50) years to rent a land @ annual rent of $(803.000). The purpose of the agreement is to build & operate a hotel, which will cost our company about $(87) million

The questions are:

1- Do we need to classify the cost of the hotel as PPE or lease?

2- What about the annual rent of the land is it operating lease or finance lease?

I’m confused as our CFO claiming to capitalized the land rent which paid during the construction period to hotel cost, after the hotels open then the rent of land is to be treat as operating lease.

Your feedback will be highly appreciated

Hi Ahmed,

1. The cost of the hotel will definitely be the PPE (it is not subject of the lease, but you construct it).

2. The rent of the land is an operating lease, because the land has an indifinite useful life. Now, whether the rent during the construction period can be capitalized or not, it’s a huge question and I tried to clarify it here. S.

Thanks a lot for the valuable inputs, really appreciated

Hi Silvia

the rent of land for 50 years appear to satisfy the fight-of-use asset – land for a period for the lessee. why is it treated as operating lease? I note that your article about states that there is no classification of operating lease and finance lease for lessee.

Thanks for sharing the video. You have made the complex IFRS 16 look easy !The moot question of double accounting of asset by both lessor and lessee remains.

Yes, Atul, you are right. It might seem a bit odd that currently, an asset is shown in both lessors’ and lessees’ accounts. S.

In fact it is not the same asset that lessor and lessee show in case of operating lease. Lessor presents PPE while Lessee has to account for his “Right to use that PPE” and that too only to the extent of what he has to pay for a rented period (not the fair value of the asset (or the carrying value of the asset in Lessor’s books) on the date of the lease). So, technically they are different.

Kamran, I never ever said that these 2 assets are the same. All I said is that yes, both lessor and lessee have an asset in their books.

You have derecognised the underlying leased Asset in the the lessor Accounts in your article by debiting receivable and in the video you taught that leased Asset should be shown in both of the financial statements?

That’s not what I taught. Please go and revise again. Thanks.

Thanks for sharing the article!

Thank you soo much.

Hi, Thank you for all the updates…!

Thank you for all

Thank you soo much

thanks for the insight

Thank you for all

Dear all

I need assistance with regards to Leaseshold improvements, do we capitalize leasehold improvements under IFRS16

Yes, you can, but not under IFRS 16 🙂 They are a separate asset under IAS 16. Just be careful about their useful life (if they are attached to the leased asset, then the useful life should not exceed the lease term).

Can you please provide a reference or is there any provision in IFRS 16 regarding this issue?

what are the reason that leasehold property is not classified Under IFRS 16,

Here lease rent is also paid, lower Purchase option also provided to convert freehold property

have also right to use , right to provide direction .

Ok if this cover under IAS 16 then it is amortized over the lease period because lessee have right only ( as intangible ) , but in our book we have shown as PPE not a Intangible assets —Why

Hi I wanted to know how to adopt IFRS 16 by following retrospective modified approach for the following items”-

1) Lease equalisation reserve

2) Advance rent paid

3) Prepaid expenses

4) Rent already paid